What Is DeFi? 2026 Complete Beginner’s Guide (Real Examples, Real Risks, Real Yields)

Table of Contents

Editorial independence & fact-check disclosure: ChainGain does not receive affiliate commission from Aave, Uniswap, Lido, Compound, Pendle, Yearn, MetaMask, Rabby, DefiLlama, or any DeFi protocol referenced. TVL, APYs, and gas fees verified 2026-05-25 via DefiLlama, protocol stats pages, and Etherscan. DeFi data changes minute-by-minute — always cross-check on DefiLlama before depositing.

Key Takeaways

- DeFi is financial services running on public blockchains via smart contracts — mainly Ethereum plus Layer 2 networks (Arbitrum, Base, Optimism). No bank, broker, or intermediary processes your trade, loan, or savings.

- Five protocol categories cover most DeFi activity: Lending (Aave $13.7B), DEX (Uniswap $3.3B), Liquid Staking (Lido $18.6B), Yield (Pendle $1.6B, Yearn), Stablecoins (Sky/MakerDAO $6.0B). TVL via DefiLlama 2026-05-25.

- Realistic 2026 yields: 3-8% APY on conservative stablecoin supply, 10-50%+ on leveraged or volatile positions (with proportional loss exposure). Bank savings rates: 0.5-5%.

- Four primary risk categories: smart contract bugs (Beanstalk $182M, 2022), oracle manipulation (Mango $116M, 2022 — trader’s convictions vacated May 2025), governance/compiler bugs (Curve $70-73.5M, 2023), regulatory action (Tornado Cash sanction 2022, lifted March 2025).

- Self-custody required — you control the wallet, read contract addresses, manage gas ($0.10-50 per transaction by chain). Lose your seed phrase, lose your funds permanently. No customer service.

- The emerging-market case is strongest: DeFi works without a bank account — matters in Nigeria, Argentina, Turkey, and the Philippines where local currencies have lost purchasing power. Stablecoin rails on Tron carry remittance costs of $0.50-2.00 per transfer (see our USDT vs USDC guide).

We’ve watched DeFi grow from a $1 billion experiment in late 2019 to an ecosystem with tens of billions locked across lending, trading, staking, and yield today. We’ve used these protocols ourselves — opened supply positions on Aave, swapped on Uniswap before V3 existed, and watched the Beanstalk flash-loan governance attack drain $182 million in a single block in April 2022.

Unlike most “What Is DeFi?” guides — written for a Wall Street audience by people who have never clicked Connect Wallet — we’ve spent two years tracking how DeFi actually works for users in Nigeria, Argentina, Turkey, and the Philippines: geographies where banking failures and currency instability make DeFi rails more than a Silicon Valley experiment, and where ChainGain publishes in 14 languages.

This guide walks through five real protocol workflows at the UI level, compares DeFi to traditional finance on eight specific axes, documents the four risk categories with verified loss events, and closes with the emerging-market case, self-custody, brief tax notes, and a 2026 trends outlook covering RWA, restaking, and modular Layer 2s.

What Is DeFi? (TL;DR for Beginners)

DeFi — short for decentralized finance — is the umbrella term for financial services (lending, borrowing, trading, savings, payments, insurance) running on public blockchains via smart contracts instead of banks, brokers, or licensed intermediaries. When you supply USDC to Aave for yield, no loan officer approves it. When you swap ETH for USDT on Uniswap, no exchange matchmaker pairs your order. The smart contract executes when its conditions are met, recorded on a public ledger. That is the entire definition; everything else is a consequence.

For the layers underneath, see our What Is Cryptocurrency? primer and What Are Stablecoins?. The U.S. Congressional Research Service’s 26-page DeFi overview (R48883) from March 2026 is the clearest non-promotional reference we’ve found.

DeFi vs Traditional Finance: 8-Axis Comparison

The simplest way to understand DeFi is to put it next to the financial system you already know. Some axes favor DeFi (yield, speed, accessibility, 24/7 operation); others favor traditional finance (consumer protection, recourse, fraud reversibility). The table summarizes the eight that matter most for a beginner.

| Axis | Traditional Finance | DeFi |

|---|---|---|

| Savings yield | 0.5-5% APY (US HYSA 4-5%, EU 1-3%) | 3-8% APY stablecoin supply; 10-50%+ leveraged/volatile |

| Fees per tx | $0-30 (wire/ACH), 1-5% FX/remittance | $0.10-2 L2; $1-50 Ethereum mainnet |

| Settlement speed | Same-day to 3-5 business days | Seconds to minutes; instant on L2 |

| KYC | Mandatory (ID, address, source-of-funds) | None at protocol layer; some frontends geo-block |

| Minimum capital | $0-500 | ~$1 principle; $50-200 practical floor on Ethereum, $10-20 on L2 |

| Custody | Custodial (bank/broker holds assets) | Self-custody (you hold private keys) |

| Recourse | FDIC/FSCS/EU deposit insurance, courts, regulators | None at protocol layer; optional insurance via Nexus Mutual |

| Operating hours | 9-5 weekdays; markets close evenings/weekends | 24/7/365; no holidays |

Two observations. The yield advantage is real on the conservative end but narrows against US high-yield savings and short-duration Treasuries; headline 50% APYs always carry leverage or smart-contract exposure. The no-recourse line is why DeFi is not a checking account replacement — but also why DeFi works for users whose checking account is unreliable, frozen, or denominated in a collapsing currency.

The 5 DeFi Categories You’ll Actually Encounter

DefiLlama tracks 3,000+ individual protocols across dozens of chains, but beginner activity falls into five categories. The table names the dominant protocol in each, its current TVL, and a representative APY range as of 2026-05-25. TVL figures via DefiLlama, our primary public source for cross-protocol comparisons.

| Category | Lead protocol | TVL | Typical APY | Risk tier | Ideal first use |

|---|---|---|---|---|---|

| Lending | Aave V3 | $13.735B | 3-8% stablecoin supply | 2 (low-med) | Supply USDC for passive yield |

| DEX | Uniswap V4 | $3.321B | N/A (swap fees) | 2 (low-med) | Token swaps without an exchange account |

| Liquid Staking | Lido | $18.571B | 2.5-4% stETH | 2 (low-med) | Stake ETH, keep liquid stETH |

| Yield / Aggregation | Pendle | $1.598B | 5-25% (market-dependent) | 3-4 (med-high) | Split principal vs yield tokens (advanced) |

| Stablecoin issuer | Sky (MakerDAO) | $5.989B | 4-8% Sky Savings Rate | 2 (low-med) | Mint DAI/USDS or earn SSR |

Lending: Aave and Compound

Lending is the entry point for most new DeFi users. You deposit (USDC, ETH, WBTC) and earn a variable APY funded by borrowers paying interest on collateralized loans. Aave V3 ($13.735B TVL — the largest lending protocol across all chains) and Compound V3 are both over-collateralized: borrowers must lock more value than they borrow, and the protocol auto-liquidates collateral if loan-to-value deteriorates. That is why DeFi lending did not collapse the way Celsius and BlockFi did in 2022.

Decentralized Exchanges: Uniswap and Curve

A DEX swaps tokens via an automated market maker (AMM) — a smart contract quoting prices from the ratio of tokens in a liquidity pool. Uniswap V4 (released early 2025) is the dominant DEX at $3.321B TVL; Curve specializes in stablecoin-to-stablecoin swaps with low slippage. No exchange account, no order book, no KYC at the protocol level. LPs earn trading fees but face impermanent loss — the cost of holding a pool position vs the underlying tokens when prices diverge.

Liquid Staking: Lido and Rocket Pool

Liquid staking lets you stake ETH (earning ~2.5-4% APR) while receiving a liquid token (stETH from Lido, rETH from Rocket Pool) usable elsewhere in DeFi. Lido alone holds $18.571B TVL — the largest single DeFi protocol, bigger than Aave or Uniswap. Detail in our Liquid Staking 2026 guide. The restaking layer above (EigenLayer, $6.551B TVL) is covered in our Liquid Restaking 2026 guide.

Yield Aggregation: Pendle and Yearn

Pendle ($1.598B TVL) and Yearn are the two recognizable names. Yearn automates moving capital between protocols; Pendle tokenizes yield-bearing assets into Principal Tokens (PT) and Yield Tokens (YT), letting users lock in fixed yields or speculate on rates. Not beginner-day-one products. Mechanics in our DeFi Vaults 2026 comparison.

Stablecoin issuers: Sky (MakerDAO) and Frax

Sky (rebranded MakerDAO) holds $5.989B TVL backing DAI and USDS and offers the Sky Savings Rate (4-8% band). Centralized issuers like Circle (USDC) and Tether (USDT) are not DeFi protocols themselves but their tokens are the dominant medium of exchange across DeFi. See our stablecoin primer and stablecoin savings rates guide.

How to Get Started in DeFi (5 Real Walkthroughs)

The protocols above are easier to use than their reputations suggest. Below are five beginner-friendly walkthroughs at the level of detail we wish we’d had in 2020. We assume you have a self-custody wallet (MetaMask or Rabby — see our wallet decision framework) and some ETH or USDC on Ethereum mainnet or a Layer 2 (Arbitrum, Base, Optimism).

Walkthrough 1: Supply USDC to Aave (earn passive yield)

Open app.aave.com, click Connect Wallet, choose Arbitrum or Base (fractional mainnet gas). From the Dashboard, find USDC in the Supply section, click Supply, enter the amount, approve the token spend (transaction 1), confirm the supply (transaction 2). You immediately start accruing yield, updating block by block. You receive an aUSDC token representing your deposit plus accrued interest; withdrawable any time. Realistic yield: 3-8% APY.

Walkthrough 2: Swap ETH for USDT on Uniswap

Open app.uniswap.org, Connect Wallet, select your network. Pick From token (ETH) and To token (USDT), enter the amount. Uniswap quotes a price including its 0.05-1% fee and your slippage tolerance (default 0.5%). Click Swap, confirm. Settlement is one transaction. Layer 2 cost: roughly $0.10-1 in gas plus protocol fee. Ethereum mainnet during congestion: $5-50 in gas alone.

Walkthrough 3: Stake ETH with Lido (get stETH)

Open lido.fi, Connect Wallet on Ethereum mainnet. Enter ETH amount, click Stake, confirm one transaction. You receive stETH 1-for-1. The stETH balance increases daily as staking rewards accrue (rebasing token). Use stETH as collateral in Aave, swap it for ETH on Curve (small spread), or hold. Unstaking to native ETH takes 1-5 days via the Lido withdrawal queue. Realistic APR: 2.5-4% net of Lido’s 10% staking fee.

Walkthrough 4: Supply on Compound V3

Open app.compound.finance, Connect Wallet, pick a market (e.g., USDC on Base). Click Supply, enter amount, approve, confirm. Nearly identical to Aave, but Compound V3 isolates each market (USDC market separate from ETH market, etc.). Yields run 3-6% APY on USDC. Compound’s risk profile is similar to Aave’s — battle-tested, multiply audited — with smaller market size.

Walkthrough 5: Lock in a fixed yield with Pendle

The most advanced of the five; try the first four first. Open app.pendle.finance, Connect Wallet. Pendle takes a yield-bearing asset (sUSDe, stETH) and splits it into a Principal Token (PT — redeemable for the underlying at maturity) and a Yield Token (YT — receives all yield until maturity). Buy PT and hold to maturity to lock in a fixed APY. Buy YT to speculate that yield stays high. Start small on short-dated markets. See our DeFi Vaults 2026 guide for full context.

Gas Fees: What You’ll Actually Pay

Gas fees are the biggest practical barrier for new users. On Ethereum mainnet a simple Uniswap swap costs $1-3 during low congestion and $30-100 during peaks (NFT launches, depeg events). Aave deposits run similar numbers.

Layer 2 networks (Arbitrum, Base, Optimism) push fees down by orders of magnitude — the same Uniswap swap typically costs $0.10-1 on L2, 10-100x cheaper than mainnet, while inheriting Ethereum security through cryptographic proofs. For beginners with under $10,000 in capital, L2 is almost always the right starting point. L2Beat tracks fees and security maturity per chain. Tron (a separate L1, not an Ethereum L2) carries the lowest USDT transfer fees at $0.50-2.00, which is why Tron-USDT dominates remittance corridors despite Ethereum’s better DeFi composability.

The 4 DeFi Risks (With Real Loss Events)

Every “What Is DeFi?” guide has a Risks section, usually five bullets ending in “do your own research.” The risks below are framed by event — specific protocols, dates, dollar amounts — because abstract “smart contract risk” doesn’t help a beginner internalize what’s at stake. The table covers the four categories every DeFi participant must understand, with one verified event per category.

| Risk type | Event | Date | Loss (USD) | Root cause | Recovery |

|---|---|---|---|---|---|

| Smart contract bug | Beanstalk Farms | 2022-04-17 | $182M | Flash-loan governance attack; one-block proposal passage and treasury drain (Bloomberg) | None |

| Oracle manipulation | Mango Markets | 2022-10-11 | $116M | Eisenberg manipulated MNGO oracle to inflate collateral; criminal convictions vacated 2025-05-23 (TRM Labs); SEC civil case ongoing | Partial (~$67M settlement) |

| Governance / compiler bug | Curve Finance reentrancy | 2023-07-30 | $70-73.5M | Vyper compiler bug v0.2.15-0.3.0 enabled reentrancy on specific pools (Chainalysis) | ~73% recovered |

| Regulatory action | Tornado Cash OFAC sanction | 2022-08-08 | N/A (access frozen) | OFAC sanctioned protocol/addresses; Fifth Circuit ruled against 2024-11-26; sanctions lifted 2025-03-21 | Sanctions fully lifted |

Smart contract bugs

Beanstalk Farms, April 17, 2022 — the canonical case. A flash loan acquired enough governance tokens (BEAN) in one transaction to pass a malicious proposal draining the $182M treasury, repaid in the same block. The flaw was design, not code — no time-lock between proposal and execution. None recovered (Bloomberg, CoinDesk, Merkle Science). Lesson: governance time-locks are not optional for nine-figure treasuries.

Oracle manipulation

DeFi protocols depend on price oracles to value collateral. Mango Markets, October 2022: Avraham Eisenberg moved the MNGO oracle upward, used inflated collateral to borrow $116M in real assets, walked away. Criminally charged and convicted April 2024 — but on May 23, 2025 Judge Arun Subramanian vacated those convictions, holding that misrepresentations to a protocol could not, as a matter of law, constitute fraud against its users (TRM Labs). SEC civil case continues. Takeaway: the legal framework is unsettled; recovery is uncertain even when an attacker is identified.

Governance attacks and compiler bugs

Sometimes the bug is in the language compiler, not the protocol. Curve Finance, July 30, 2023: a Vyper compiler bug (versions 0.2.15-0.3.0) enabled reentrancy on specific pools (Chainalysis); $70-73.5M drained, ~73% recovered through white-hat front-running and negotiation. Compiler bugs are rare but hard to defend against — a protocol can have a perfect audit and still be exposed if the underlying tooling has a flaw. Euler Finance, March 13, 2023 ($197M flash loan, $240M later recovered per Chainalysis and Fortune) is another instructive case.

Regulatory action

Tornado Cash OFAC sanction, August 8, 2022: illegal for US persons overnight. On November 26, 2024 the Fifth Circuit ruled against the sanction, finding smart contracts cannot be “property” sanctioned under the statute. On March 21, 2025, sanctions were officially lifted. Regulatory risk is active and fast-moving, capable of affecting protocol access even when the protocol has no technical flaws. SEC, EU MiCA, and national regulators continue to evolve DeFi guidance.

Rug pulls are a fifth category, but the beginner-relevant protocols above are not rug candidates — they are years old, multi-audit, with public teams and large on-chain treasuries. Rugs dominate meme-coin and “high-yield” farm spaces; the Squid Game token rug of November 1, 2021 ($3.4M per Washington Post, some sources up to $11.9M) is the canonical reminder that “high APY + new protocol + anonymous team” is the most reliable rug pattern. Rekt News is the public reference for hack/rug history.

Disclaimer (Risk Matrix caption restatement): The protocols named have substantial audit coverage, bug bounties, and operational history. Historical events in Table 3 are not claims about current risk — they illustrate the categories that exist in DeFi as a whole. Verify any protocol on DefiLlama before depositing.

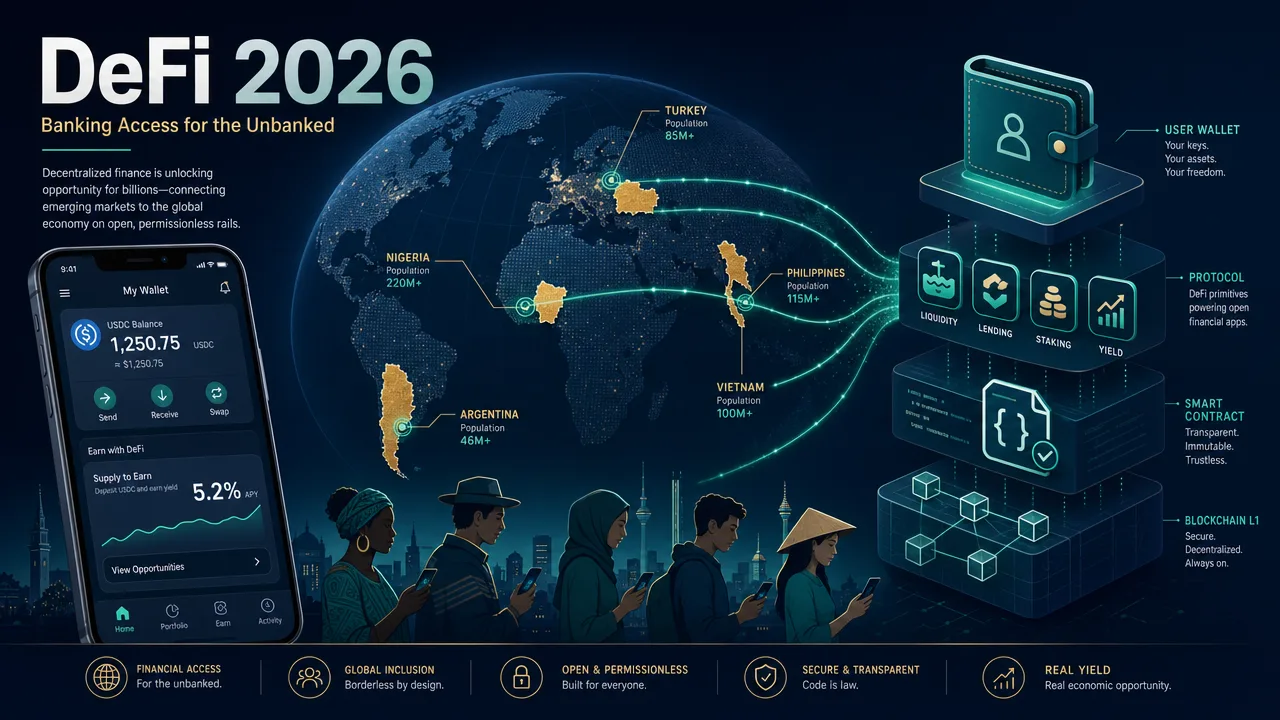

DeFi for Emerging Markets: Banking Access for the Unbanked

The strongest case for DeFi — the one most “What Is DeFi?” guides miss — is banking access for users whose local system is unreliable, restrictive, or denominated in a depreciating currency. The Chainalysis Global Crypto Adoption Index (2025) ranks Nigeria, India, Vietnam, the Philippines, Argentina, and Turkey near the top. The reasons are practical, not speculative.

Argentina: inflation hedge via stablecoins

Argentina has had extended periods of triple-digit annual inflation in the 2020s. Pesos in a local bank guarantee loss of purchasing power; dollar account access is restricted by capital controls. USDT or USDC in self-custody — earning 3-8% in DeFi lending — is not speculative here. It is a dollar-denominated savings account the local system does not provide. Risks are weighed against certain peso depreciation, not against an insured US account.

Turkey: stablecoin demand against lira weakness

The lira has lost significant value against the dollar with annual inflation well above developed-market norms. Domestic USDT appetite has grown accordingly; the DeFi yield premium over zero-interest checking is meaningful when local savings cannot keep up with cost-of-living.

Nigeria: stablecoin payments and P2P rails

Africa’s highest per-capita crypto adoption, driven by remittance demand and dollar scarcity for businesses paying international suppliers. Stablecoin P2P markets settle in minutes at a small spread above the bank rate; DeFi lending and Curve swaps fit naturally into the existing P2P workflow.

Philippines: remittances and payroll

One of the world’s largest remittance recipients. USDT on Tron or USDC on L2 settles in minutes at $0.50-2.00 per transfer vs variable WU fees. Some Filipino payroll services pay overseas workers in USDT directly. See Crypto vs Western Union and our USDT vs USDC remittance guide.

Disclaimer (Emerging Market section restatement): DeFi use in the jurisdictions above is subject to local law and may be restricted, taxed, or affected by regulatory changes. Consult local counsel before relying on DeFi rails for material savings.

DeFi and Remittances: How Stablecoin Rails Beat Western Union (Sometimes)

One of the most concrete DeFi-adjacent use cases is cross-border remittance. Through Western Union, costs vary by corridor and method — our crypto vs Western Union analysis documents WU online transfers in the 1-3% range for some corridors, with higher all-in costs (4-5%+) for smaller transfers. Crypto rails are not always cheaper — but the lowest-cost rails (USDT on Tron) commonly come in around $0.50-2.00 per transfer regardless of amount per our KG-1 USDT vs USDC analysis. For larger transfers ($5,000+), the percentage savings compound meaningfully.

The catch is off-ramp: the recipient must convert USDT back to local currency, depending on local infrastructure. In Nigeria, the Philippines, and Argentina, robust P2P markets make this practical. Elsewhere, off-ramp friction can erode the savings. Stablecoin rails are often cheaper than Western Union, almost always faster, and almost always more transparent — but the exceptions are real. Use the calculator above to model your corridor.

Self-Custody Reality: What “Be Your Own Bank” Actually Means

DeFi requires self-custody — you hold the private keys. No bank, no exchange account, no customer service. Marketing presents this as a feature (“be your own bank!”) and it is — but it is also the source of permanent, irrecoverable failure modes beginners regularly underestimate.

The seed phrase

Wallets generate a 12 or 24-word seed phrase — the master key to every account. Anyone with the phrase has the funds. If you lose it, funds are gone forever (no recovery, no support, no insurance). Write it down (never digitally), store it fire/water-resistant, back up in a second location. This is the most important operational discipline in DeFi.

Hardware wallets

For amounts above ~$1,000, a hardware wallet (Ledger, Trezor) is strongly recommended. The device keeps the private key on dedicated hardware and signs without exposing it to your computer. Cost: $80-150. Benefit: substantial attack-surface reduction.

Multi-sig and social recovery

For $10,000+, multi-signature wallets (Safe, formerly Gnosis Safe) require multiple keyholders to approve transactions. ERC-4337 account abstraction supports social recovery — designated guardians can collectively reset a lost key. Both add complexity but reduce single-point-of-failure risk.

Full decision framework: wallet decision framework. Also review the USDT frozen by Tether recovery guide — even self-custody stablecoins carry issuer counterparty risk; Tether can blacklist USDT in any wallet by design.

Disclaimer (Self-custody section restatement): Loss of a seed phrase or unauthorized wallet access = permanent loss of funds with no recovery path. There is no FDIC equivalent. Do not skip the hardware wallet upgrade for material amounts.

DeFi Tax Treatment (Brief)

DeFi tax treatment varies by jurisdiction and is one of the under-discussed costs of participation. In the US, DeFi yield (lending interest, staking rewards, LP fees) is generally ordinary income at receipt, while token swaps and disposals trigger capital gains or losses. Some protocols issue 1099-MISC for clearly-attributable yield; others issue nothing. Auto-compounding vaults create dozens or hundreds of taxable events per year that are painful to reconstruct after the fact.

EU treatment under MiCA and member-state codes varies; the UK treats most DeFi yield as miscellaneous income with capital gains on disposal. For full US/UK/DE/AU/JP coverage see our crypto capital gains tax 2026 guide. Honest summary: track everything from day one, use a crypto tax tool from your first transaction, and budget for year-end reconciliation time. The IRS, HMRC, and most national tax authorities are increasing DeFi enforcement, not decreasing it.

2026 DeFi Trends: RWA, Restaking, Modular L2s

Three trends define the 2026 DeFi landscape and shape where capital is flowing. All three create new opportunities and new risk surfaces.

Real World Assets (RWA)

RWA tokenization wraps off-chain assets (Treasuries, real estate, private credit) as on-chain tokens. Ondo, Maple, and Centrifuge offer exposure to tokenized T-bill yields (4-5% APY) or private credit (8-12% with credit risk). Benefit: composability — RWA tokens can be collateral or DEX-paired. Risk: new off-chain counterparty failure mode, including custodian failure and legal disputes between on-chain holders and off-chain owners.

Restaking

Restaking protocols (EigenLayer, $6.551B TVL per DefiLlama 2026-05-25) let stakers reuse staked ETH as security for bridges, oracles, and DA layers. Yield premium is real (5-15% APY layered on base staking) but slashing can now be triggered by misbehavior at any secured service. Mechanics in our Liquid Restaking 2026 guide.

Modular Layer 2s and the cost collapse

The modular L2 thesis — separating execution, settlement, and data availability — has driven transaction costs down by orders of magnitude. Arbitrum, Base, and Optimism routinely settle DeFi transactions for $0.10-1; newer L2s (Mantle, Linea, Scroll) push further. Effect: DeFi is increasingly affordable for retail sizes ($100-1,000) that were uneconomic on mainnet two years ago. Trade-off: fragmentation — capital lives on a specific chain, bridging adds bridge-operator counterparty risk. L2Beat remains the public reference for L2 security and cost.

How to Stay Safe in DeFi (Checklist)

Most DeFi losses to retail users are not exotic exploits — they are basic operational mistakes. The checklist below covers the high-leverage habits that prevent the most common failures.

- Verify the website URL every time. Bookmark the official protocol site after one careful verification (cross-check on DefiLlama). Phishing copies of Aave, Uniswap, and Compound proliferate in Google ads and on X.

- Start small. Your first deposit on a new protocol should be the smallest amount that completes a full deposit-and-withdraw round trip — $10-50, not $1,000.

- Read the contract address you’re approving. “Unlimited spending of USDC” grants the contract permission to move your USDC forever. Revoke unused approvals via

revoke.cash. - Hardware wallet for amounts above $1,000. $80-150 cost; enormous attack-surface reduction.

- Back up your seed phrase in two physical locations. Never digitally. Never as a photo. Never in a password manager.

- Verify TVL and audit status on DefiLlama before depositing. Under $50M TVL or no major audits = significantly higher risk than Table 2 names.

- Diversify across protocols, not just tokens. $50K USDC entirely in Aave is one concentrated smart-contract risk; splitting across Aave and Compound diversifies it.

- Check for frontend geo-blocks before bridging large amounts. Several DeFi frontends block US/UK/sanctioned-jurisdiction IPs at the UI layer.

- Track taxes from day one. Crypto tax software (Koinly, CoinTracker, TokenTax) is dramatically easier than year-end reconstruction.

FAQ

Is DeFi the same as cryptocurrency?

No. Cryptocurrency is the token layer (BTC, ETH, USDT, USDC) and the blockchains they run on. DeFi is the application layer of financial services built on top. You can hold crypto without using DeFi (wallet or exchange). You cannot use DeFi without crypto in a self-custody wallet. See our What Is Cryptocurrency? primer.

Is DeFi safe for beginners?

“Safe” is relative. Protocols with the longest history and most audit coverage (Aave, Uniswap, Lido, Compound, Sky) have substantially better safety records than newer or smaller ones — but none is exploit-proof. Recommended: start with $50-200 on a Layer 2, supply USDC to Aave or Compound to learn the wallet flow, scale up only after several months at small size without losses.

How much money do I need to start using DeFi?

In principle $1; in practice gas fees set the floor. Ethereum mainnet transactions cost $5-50, so deposits under $200 are usually uneconomic. Layer 2 transactions cost $0.10-1, so $20-50 deposits make sense. We recommend $100-500 for your first real DeFi experience on Layer 2.

What’s the difference between DeFi and a centralized exchange like Coinbase or Binance?

Centralized exchanges (CEX) are custodial — they hold your crypto. DeFi protocols are non-custodial — you hold your own keys. CEX is easier and has support but can freeze your account, go insolvent (FTX, Celsius), or be seized. DeFi gives full control but no safety net.

Can I lose all my money in DeFi?

Yes — via smart contract exploit, private key loss, phishing (signing a malicious approval), or leveraged liquidation. The Stay Safe checklist reduces but does not eliminate risk. Never deposit more than you can afford to lose.

Is DeFi legal where I live?

DeFi participation is legal in most jurisdictions, but specific activities can be restricted. The US OFAC Tornado Cash sanction (2022-2025, now lifted) is the highest-profile example. EU MiCA is extending licensing requirements to some DeFi activity. Some frontends geo-block specific jurisdictions. Check local regulations and consult counsel before material amounts. The CRS 2026 DeFi overview (R48883) is a useful US starting point.

Continue Learning

- Best Stablecoin Savings Rates 2026 — CeFi vs DeFi yield baseline (S1)

- Liquid Staking 2026: Lido vs Rocket Pool vs Frax — Deep dive into the largest single DeFi category (DF-1)

- Liquid Restaking 2026: EigenLayer vs Symbiotic vs Karak — The slashing risk layer above LSTs (DF-2)

- DeFi Vaults 2026: Yearn vs Beefy vs Convex vs Pendle — Risk-adjusted yield aggregator comparison (DF-3)

- What Are Stablecoins? — The token layer powering most DeFi activity (Art4)

- What Is Cryptocurrency? — Foundation primer for the blockchain layer (Art1)

- USDT vs USDC: Best Stablecoin for Remittances 2026 — Corridor-by-corridor cost analysis (KG-1)

- Crypto Wallet Decision Framework 2026 — Choosing self-custody for your holding size (W-2)

Crypto Analyst at ChainGain

ChainGain author since 2026. Alex has covered cryptocurrency markets and blockchain technology since 2019, with a focus on practical guides for users in emerging markets where DeFi rails solve real banking and remittance problems. He has used Aave, Uniswap, Compound, Lido, and Pendle continuously since 2020 and tracks every DeFi exploit listed in the Rekt News leaderboard. Full bio.

Disclaimer: This article is independent. ChainGain does not receive affiliate commission for Aave, Uniswap, Lido, Compound, Pendle, Yearn, MetaMask, Rabby, DefiLlama, or any DeFi protocol mentioned. TVL, APYs, and gas fees verified 2026-05-25 via DefiLlama, protocol stats pages, and Etherscan — DeFi metrics change minute-by-minute; verify on defillama.com or the protocol dashboard before decisions. Not investment advice: DeFi carries smart contract bug risk (whole protocol can be drained), oracle attack risk, governance attack risk, and evolving regulatory risk (SEC, MiCA may restrict access). Self-custody warning: losing your seed phrase = permanent loss with no recovery path. Geographic restrictions: some protocols block US/UK/sanctioned-jurisdiction users at the frontend. Past hack examples (Beanstalk, Mango, Squid Game, Tornado Cash, Curve, Euler) are historical; this does not imply current protocols carry equivalent risk — most listed protocols have substantial audits and bug bounties, but no protocol is exploit-proof.

Part of ChainGain’s What Is DeFi? Decentralized Finance Explained for Beginners (2026) guide series.