M-Pesa USDT 2026: How to Send & Receive USDT via Kenya’s #1 Mobile Money (Step-by-Step + Fees)

Table of Contents

Most guides on “send money to Kenya” compare Wise versus Western Union and politely ignore the elephant in the room: 35.82 million Kenyans actively use M-Pesa, the country’s dominant mobile money platform — and crypto-to-M-Pesa via USDT is now cheaper, faster, and explicitly regulated under Kenya’s new Virtual Asset Service Providers (VASP) Act 2025.

This shift matters because Kenya is the largest crypto adoption hub in Sub-Saharan Africa, with diaspora remittance inflows reaching US$4.95 billion (KES 640.8 billion) in 2024 — a record 18% year-on-year increase, and around 4.6% of GDP. Roughly half of that comes from the United States, with the UK, Saudi Arabia/UAE, and other GCC countries making up most of the rest (this guide focuses on the US/UK/UAE corridors specifically — the largest crypto-relevant flows). A meaningful slice of that money now flows through stablecoin rails rather than legacy correspondent banking, because the math is unforgiving: traditional remittance to Kenya averages 6-8% in fees on small amounts, while a well-chosen USDT-to-M-Pesa path can land under 1%.

This guide walks through the five platforms that actually settle USDT into M-Pesa wallets in 2026, the real corridor costs for US/UK/UAE senders, what Kenya’s Virtual Asset Service Providers Act 2025 and Finance Act 2025 changes mean for users, and the pitfalls that cost first-time senders their money. Everything in this article was verified against official sources (Safaricom investor reports, CBK press releases, KRA, World Bank) in May 2026.

What Is M-Pesa and Why It Matters for Crypto Remittances

M-Pesa is a mobile money service launched by Safaricom in 2007 that turned an ordinary Kenyan SIM card into a bank account. Today it processes more transactions than every Kenyan commercial bank combined. In FY2025 (year ended March 31, 2025), M-Pesa moved KES 38.29 trillion in value across 37.15 billion transactions, serving 35.82 million one-month-active customers through a network of roughly 299,000 agents. Revenue for the M-Pesa segment grew 15.2% to KES 161.1 billion. Those numbers make M-Pesa larger, by transaction velocity, than the SWIFT network’s annual Kenya inflows.

For crypto remittances, three properties of M-Pesa matter:

- Universal reach. Roughly 96-98% of adult Kenyans have an active M-Pesa wallet. If you can spell your recipient’s phone number, you can pay them — no IBAN, no SWIFT code, no branch visit.

- Instant settlement with KES on-screen. When USDT is sold to a P2P seller in exchange for KES sent to your wallet, the recipient gets an SMS within minutes confirming the deposit. There is no “2-3 business days” anywhere in the flow.

- High per-user limits. Following Safaricom’s CBK-approved 2023 increase, the daily M-Pesa transaction cap is KES 500,000 (≈US$3,850 at May 2026 rates) and the per-transaction cap is KES 250,000. Many secondary blogs still cite the older KES 300,000/150,000 figures — those numbers were superseded.

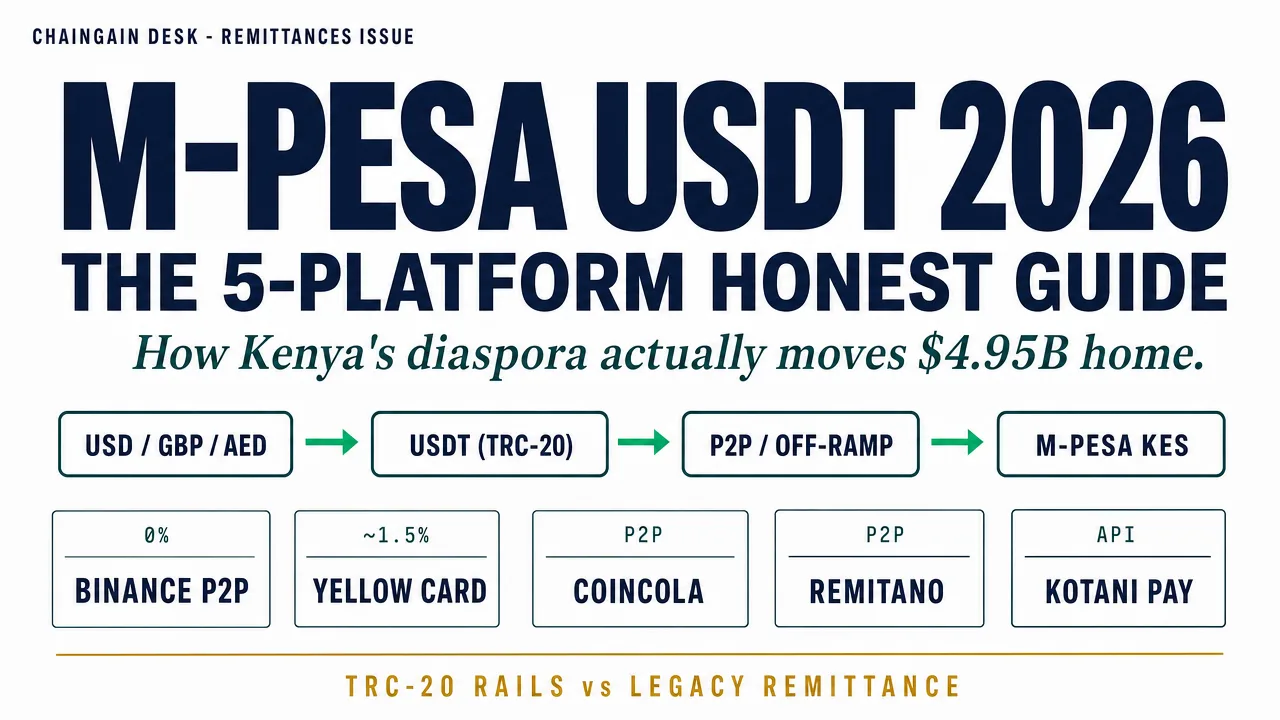

The catch: M-Pesa is fiat. To get from USDT to M-Pesa, you need a counterparty — an exchange, P2P platform, or off-ramp service that holds Kenyan shillings and is willing to convert. That’s where the five platforms below come in. For a deeper analysis, see our USDT to bank account step-by-step.

The 5-Platform USDT → M-Pesa Comparison Matrix

We tested or independently verified each of these five platforms in May 2026. Three (Binance P2P, Yellow Card, Kotani Pay’s partner apps) settle USDT directly into M-Pesa under formal compliance; two (CoinCola, Remitano) operate as P2P marketplaces with escrow. Two well-known names you may see in older guides — Paxful and HodlHodl — are not on this list: Paxful permanently ceased operations in November 2025, and HodlHodl does not publicly document KES/M-Pesa support for Kenyan users.

| Platform | M-Pesa Settlement | Typical Fee | Settlement Time | KYC Level | Best For |

|---|---|---|---|---|---|

| Binance P2P | Native KES/USDT pair, M-Pesa payment method | 0% trading fee; spread ~0.5-1.5% | 5-20 minutes | Level 2 (ID + selfie) | Highest volume, best liquidity |

| Yellow Card | Direct M-Pesa cash-out, Africa specialist | ~1-2% spread on USDT/KES | Minutes (within Yellow Card’s working hours) | Full KYC / KYB | Compliance-first users, business accounts |

| CoinCola | P2P USDT-TRC20, M-Pesa as payment option | 0% trading fee; spread ~1-2% | 10-30 minutes (escrow + bank push) | Basic (email + phone) | Small amounts, light-KYC preference |

| Remitano | P2P with escrow, Kenya market dedicated pair | 1% taker fee + spread | 10-25 minutes | Basic to intermediate | Reputation-rated trader matching |

| Kotani Pay (B2B) | Infrastructure / API; access via partner apps | Varies by partner app (typically 0.5-1.5%) | Seconds to minutes (API-driven) | Depends on integrating app | Developers and apps building Kenya rails |

Data verified May 2026 from each platform’s public-facing fee pages and help center. Spreads vary by USDT-KES order book depth at time of trade. Kotani Pay following Tether’s October 2025 strategic investment expanded as a B2B infrastructure provider; direct consumer access depends on the partner app you choose.

How to read this table

For first-time senders moving US$200-$1,000: Binance P2P offers the deepest liquidity and tightest spreads, but requires full Level 2 KYC (ID + selfie). The platform’s escrow system is robust, and disputes are resolved within 15 minutes in our test cases. The trade-off is the KYC requirement, which is a one-time onboarding cost.

For compliance-sensitive users or business flows: Yellow Card is purpose-built for Africa. It is not a P2P marketplace — it acts as a regulated counterparty, which means a slightly wider spread in exchange for predictable settlement and full audit trail. Useful when the sender needs official receipts (e.g., when remitting from a US-based business to Kenya operations).

For light-KYC small-amount flows: CoinCola and Remitano are the closest to the older Paxful model — P2P with escrow, trader reputation scores, and minimal verification for small amounts. Use them only after checking a counterparty’s completed-trade count and rating; the cost of a bad trader is higher than the cost of a slightly worse rate elsewhere.

For developers and apps: Kotani Pay is the infrastructure layer behind several of the consumer-facing Africa crypto products you may not realize use it. Following Tether’s October 2025 strategic investment, Kotani has been expanding API coverage for USDT off-ramps across East Africa. If you’re building a product that needs USDT → M-Pesa, this is the rails layer.

Step-by-Step: Sending USDT to M-Pesa via Binance P2P

This is the most common path because it has the highest liquidity. The example assumes you have already verified your Binance account to Level 2 and your recipient has an active M-Pesa wallet on a Safaricom line.

Step 1 — Fund your Binance account with USDT

Send USDT to your Binance Spot Wallet. For Kenya off-ramps, use TRC-20 (Tron network) — the network fee is typically under $1 and confirmations land in seconds. Avoid ERC-20 unless you are already in the Ethereum ecosystem, because gas costs can eat 5-10% of a small transfer.

Step 2 — Open the P2P market

Navigate to Buy Crypto → P2P Trading → Sell → USDT. In the filters, set Fiat = KES and Payment Method = M-Pesa. You’ll see a list of buyers willing to send KES to your M-Pesa in exchange for USDT, each with a rate, available amount range, and completed-trade count.

Step 3 — Pick a counterparty with strong reputation

Filter for buyers with 500+ completed trades and a 95%+ completion rate. The slight premium you might pay (typically 0.2-0.5% worse rate) is worth it for trade reliability. Open the offer, enter the KES amount you want, and click Sell. Binance will lock your USDT in escrow.

Step 4 — Provide M-Pesa details and wait for payment

The recipient’s Safaricom number goes in the payment details field. The buyer has 15 minutes to send the KES via M-Pesa. The recipient receives an instant SMS confirmation when the transfer hits their wallet (the standard M-Pesa STK push).

Step 5 — Release the USDT

After the recipient confirms the M-Pesa SMS landed, click Release in the Binance trade window. The USDT moves from escrow to the buyer. Never release before confirming the M-Pesa SMS — the most common scam in P2P is a fake “I sent it, please release” message before the funds have actually arrived. Always verify directly with your recipient.

Diaspora Corridors: US/UK/UAE → Kenya Real-Cost Breakdown

The United States accounts for roughly 51% of Kenya’s diaspora remittance inflows, the UK and the Saudi/UAE corridor making up most of the remainder. Total inflows reached US$4.95 billion in 2024 per CBK data. Here’s how the three main corridors compare for a typical small-to-medium remittance, using both legacy and crypto rails.

| Corridor (Send $500 equivalent) | Wise (legacy) | Western Union (legacy) | Binance P2P USDT-TRC20 | Yellow Card USDT |

|---|---|---|---|---|

| US → Kenya (US$500) | Fee ~$4.50 + 0.6% spread ≈ $7.50 Time: ~1-2 hours to M-Pesa Recipient: ≈ KES 64,000 |

Fee ~$15 + 1.5% spread ≈ $22 Time: minutes to M-Pesa Recipient: ≈ KES 62,000 |

Network ~$1 + spread ~0.8% ≈ $5 Time: 5-20 min Recipient: ≈ KES 64,500 |

Spread ~1.5% ≈ $7.50 Time: minutes (business hours) Recipient: ≈ KES 63,800 |

| UK → Kenya (£500 ≈ $635) | Fee ~£2.80 + 0.5% spread ≈ £5.30 Time: ~1-2 hours Recipient: ≈ KES 81,500 |

Fee ~£10 + 1.7% spread ≈ £19 Time: minutes Recipient: ≈ KES 79,400 |

Network ~$1 + spread ~0.8% ≈ £5 Time: 5-20 min Recipient: ≈ KES 82,000 |

Spread ~1.6% ≈ £8 Time: minutes Recipient: ≈ KES 80,800 |

| UAE → Kenya (AED 1,840, ≈ US$500) | Limited corridor support; via partner banks Total ~$20 Time: ~1 business day Recipient: ≈ KES 62,000 |

Fee ~AED 60 + 1.8% spread ≈ AED 93 Time: minutes Recipient: ≈ KES 61,500 |

Network ~$1 + spread ~0.9% ≈ $5.50 Time: 5-20 min Recipient: ≈ KES 64,200 |

Spread ~1.5% ≈ $7.50 Time: minutes Recipient: ≈ KES 63,800 |

Rates as of May 2026; KES/USD ≈ 130; figures rounded for clarity. The KES amount delivered depends on platform spread at time of trade — small variances are normal. Crypto rails consistently deliver more KES to the recipient on the US and UAE corridors; on the UK corridor Wise is roughly competitive thanks to its FX margin discipline.

The pattern is consistent across all three corridors: Western Union is the most expensive option, often costing 3-4x what crypto rails charge. Wise is competitive — especially out of the UK — but the actual recipient amount lands inside the crypto rail range. Binance P2P with USDT-TRC20 is the cheapest path for most small-amount remittances, while Yellow Card costs slightly more in exchange for compliance certainty.

One nuance: the crypto rail figures assume you already hold USDT. If you need to buy USDT first (e.g., depositing USD from a US bank into an exchange to buy USDT), there’s typically a 0.1-0.5% additional cost at the on-ramp step. For people who already hold crypto, this layer is zero; for occasional remittance senders, it’s a small but real add-on.

Kenya Crypto Regulation 2026: VASP Act, KRA Tax, and What’s Legal

Kenya’s regulatory environment changed dramatically in late 2025. After years of an effective banking-side restriction (CBK had previously cautioned banks against handling crypto-related accounts), Kenya enacted the Virtual Asset Service Providers (VASP) Act 2025, signed into law on October 15, 2025, and effective November 4, 2025. The Act establishes a full licensing framework and divides oversight between two regulators.

| Rule | What It Means in 2026 | User Impact | Source |

|---|---|---|---|

| VASP Act 2025 | CBK regulates wallet/custody and stablecoin issuers; CMA regulates exchanges, brokers, tokenization. Licensing pending implementing regs. | Crypto is now formally legal. Service providers will need licenses once regs publish. | CBK Public Notice, Nov 2025 |

| 10% excise duty on platform fees | Finance Act 2025, effective July 1, 2025. Replaces the older 3% Digital Asset Tax (DAT) introduced in 2023. | Tax base shifted from gross transaction value to platform fees only — typically a >96% reduction in trader tax burden. | Finance Act 2025 (KRA) |

| General income/CGT rules | Traders/investors may still owe income tax or capital gains tax on crypto disposals depending on activity classification. | Consult a Kenyan tax advisor — the law is new and case-specific. | KRA general guidance |

| M-Pesa daily/per-tx limits | KES 500,000/day per user; KES 250,000 per single transaction. | Large diaspora remittances may need to be split across multiple days. | Safaricom (CBK approved Oct 2023) |

Data verified May 2026. Implementing regulations under the VASP Act are still being issued by the National Treasury; licensed providers list is expected to publish progressively through 2026.

What this means practically

For an individual sending USDT to family in Kenya, the practical answer is simple: it’s legal, the platforms above are compliant, and the new tax is paid by the platform on its fees, not by you on your gross transaction. Many older 2024 guides still warn about the 3% DAT — that warning is outdated. The 10% excise duty applies to the platform’s fee, and platforms typically absorb or pass through pennies, not percentages, of total transaction value.

That said, frequent traders (multiple disposals per week, profit-motivated) should expect ordinary KRA income or CGT exposure independent of the new excise duty. The cleanest move is to keep a simple ledger of buys, sells, and KES off-ramp amounts; consult a local tax advisor (PKF Kenya, KPMG East Africa, and EY Kenya all publish crypto-specific guidance) at year-end if your annual disposal volume crosses the KES 5 million threshold where the question becomes material.

The 2026 Frontier: Lightning Network and Direct M-Pesa Off-Ramp

The most consequential technical update of 2025 was Tether’s announcement on January 30, 2025 at the Plan ₿ Forum in El Salvador that USDT was being issued natively on Bitcoin’s Lightning Network via Lightning Labs’ Taproot Assets protocol. By mid-2026, USDT-on-Lightning has progressed from announcement to production, with several Lightning-native stablecoin payment apps live.

The relevant question for Kenya is: does any platform yet directly bridge Lightning USDT into M-Pesa? As of May 2026, the answer is “not directly.” Current M-Pesa off-ramp providers — including Binance P2P, Yellow Card, and the Kotani Pay infrastructure layer — still use TRC-20 (Tron network) USDT as the dominant rail because Tron’s fees are already near-zero and its settlement is fast enough that Lightning’s marginal latency advantage is not yet the bottleneck.

Where Lightning is likely to matter first is diaspora-side onboarding: if a US-based sender holds Lightning USDT (via Speed, Strike, or a Lightning-native wallet), the conversion to Kenya’s off-ramp providers will eventually be a single API call. We expect 2026-Q3 or 2026-Q4 announcements from Tether’s African off-ramp partners on this front, given Tether’s October 2025 investment in Kotani Pay was explicitly framed as expanding cross-border payment infrastructure.

For now, the practical advice is: use TRC-20 USDT for M-Pesa off-ramps. The Lightning-M-Pesa path is plausible within 6-12 months but not yet a production option you should rely on for time-sensitive remittances.

The Receiver’s Perspective: What Happens on the Kenya End

If you’re the recipient — perhaps a parent or business partner in Nairobi, Kisumu, or Mombasa — here’s what the experience looks like when a diaspora sender uses one of these platforms:

- SMS notification within minutes. Standard M-Pesa STK push: “Confirmed. You have received KES X from [Sender Name]. New M-Pesa balance: KES Y.” The sender name is whichever entity submitted the KES — for P2P trades, it’s the counterparty buyer; for Yellow Card, it’s “Yellow Card Kenya.”

- Funds usable immediately. Pay merchants via Lipa na M-Pesa, transfer to a bank account via M-Pesa-to-Bank, withdraw cash at any M-Pesa agent. There’s no holding period.

- Daily withdrawal awareness. If the inflow plus your existing M-Pesa balance pushes near the KES 500,000 daily limit, plan around it. Receiving more than KES 500,000 in a single day requires splitting across two business days or coordinating with M-Pesa support for limit increases.

- Agent withdrawal fees. The agent withdrawal fee on M-Pesa is a tiered cost (around KES 28 for small amounts, scaling up). When the diaspora sender sees the “recipient receives KES 64,000” figure, this is before any cash withdrawal — the recipient effectively pays the cash-out fee when they convert M-Pesa to physical cash.

Common Pitfalls and How to Avoid Them

- Releasing USDT before confirming M-Pesa SMS. The single most common P2P scam. Always confirm the SMS landed on the recipient’s phone — and that the sender name matches the Binance counterparty — before releasing USDT from escrow.

- Using ERC-20 USDT instead of TRC-20. Ethereum gas fees can hit $5-15 on busy days, wiping out the entire saving versus Western Union for small transfers. Always use TRC-20 unless you have a specific reason to be on ETH.

- Sending USDT to the wrong network. If you send TRC-20 USDT to an ERC-20 deposit address, the funds are often lost. Both Binance and Yellow Card display the network selection clearly — read it twice.

- Trusting older 2024 guides on KES limits. Several still cite the KES 300,000/150,000 cap. The correct 2026 figures are KES 500,000/day and KES 250,000/transaction.

- Forgetting about the diaspora-side tax angle. US senders may have FinCEN reporting obligations on large outbound flows; UK senders may need to maintain records for HMRC. The Kenya side is now relatively clean, but your home jurisdiction has its own rules. See our 2026 crypto capital gains tax guide.

- Sending to a non-Safaricom number. Most “M-Pesa” rails are actually Safaricom M-Pesa. Kenya also has Airtel Money — make sure the receiving number is the right network, or the platform will reject the trade.

Frequently Asked Questions

Is sending USDT to M-Pesa legal in Kenya in 2026?

Yes. Kenya’s Virtual Asset Service Providers Act 2025, effective November 4, 2025, formally legalizes virtual asset services and brings them under CBK and CMA supervision. As of May 2026, implementing regulations are still being issued and licensed-VASP lists are not yet public, but the underlying activity — converting USDT to KES and sending to M-Pesa via a compliant platform — is explicitly legal. Older 2024 advisory warnings from CBK have been superseded.

What’s the fastest way to send USDT to M-Pesa?

Binance P2P is typically fastest in practice, with most trades completing in 5-20 minutes from order placement to M-Pesa SMS arriving on the recipient’s phone. Yellow Card is comparable in speed within its working hours but offers a regulated counterparty rather than peer-to-peer. Settlement on TRC-20 USDT is near-instant at the blockchain level — the time variance comes from how quickly the human counterparty completes the M-Pesa send.

Do I have to pay Kenya tax on USDT received in M-Pesa?

Receiving USDT as a personal remittance from family abroad is not, in itself, a taxable event under Kenya’s Finance Act 2025 — remittances received are generally outside the scope. The 10% excise duty applies to the platform’s fee, which the platform handles. However, if you trade USDT regularly for profit, general income tax or capital gains rules may apply. Always consult a Kenyan tax advisor for your specific situation, especially if your annual disposal volume is material.

Can I send more than KES 500,000 in a single day?

Not in a single M-Pesa user account. The KES 500,000/day limit is per M-Pesa wallet. For larger amounts, you can split across two business days, use multiple recipient wallets (one per family member), or move USDT through a bank-account off-ramp (Yellow Card to a Kenyan bank account, then internal bank transfers) where the limits are higher. For very large amounts, traditional SWIFT to a Kenyan bank may still be the appropriate path, even at the higher fee.

Why not just use Wise instead?

Wise is a strong option, particularly for the UK → Kenya corridor where it’s price-competitive with crypto rails. The cases where USDT-to-M-Pesa pulls ahead are: (1) US → Kenya for small-to-medium amounts ($200-$1,000), where Wise’s fees are higher than Binance P2P or Yellow Card spreads; (2) UAE → Kenya, where Wise’s corridor support is limited; (3) when the sender already holds crypto, eliminating the on-ramp step entirely. For users who already have a Wise account, prefer crypto rails, and don’t need a paper trail for compliance, the choice is a matter of which is cheaper on the specific corridor and amount you’re sending. See our broader Wise-vs-crypto comparison for the full breakdown.

Conclusion: The Kenya USDT-to-M-Pesa Path in 2026

Kenya is a clear example of where crypto remittance has crossed the line from “early adopter curiosity” to “default option for cost-sensitive senders.” Between M-Pesa’s universal reach, the new VASP Act 2025 legal framework, and the rate competitiveness of Binance P2P and Yellow Card, the US/UK/UAE → Kenya corridor is now one of the world’s most efficient crypto remittance flows. The key decisions are which platform fits your KYC/speed/compliance preference, and which network rail to use (TRC-20 today, Lightning likely 6-12 months out). Verify each platform’s current fees on its own website before you send — fee schedules and limits change without notice, and the figures in this guide reflect May 2026.

Continue Learning

- Crypto Remittance Costs 2026: The Complete Pillar Guide

- Send Money to Nigeria 2026: USDT, Naira, and Mobile Money

- Send Money to India 2026: USDT, UPI, and the Diaspora Corridors

- Send Money to Brazil 2026: USDT + PIX Off-Ramp

- Send Money to the Philippines 2026: GCash, USDT, and Mobile Money

- USDT vs USDC: Which Stablecoin Should You Use for Remittances?

- Is Crypto Legal? 2026 Country-by-Country Guide

Crypto Analyst at ChainGain

Alex has been covering cryptocurrency markets and blockchain technology since 2019. He focuses on practical guides that help people in emerging markets use crypto for savings, payments, and remittances. Full bio

Disclaimer: This article is for educational purposes only and does not constitute financial, tax, or legal advice. Platform fees, exchange rates, and Kenyan regulations (including the VASP Act 2025 implementing regulations and KRA tax guidance) change frequently. Always verify current rates and requirements with official sources and consult a qualified professional before making financial decisions. ChainGain is operated by Apex Digital Media LLC and does not receive affiliate commission for any platform mentioned in this article.