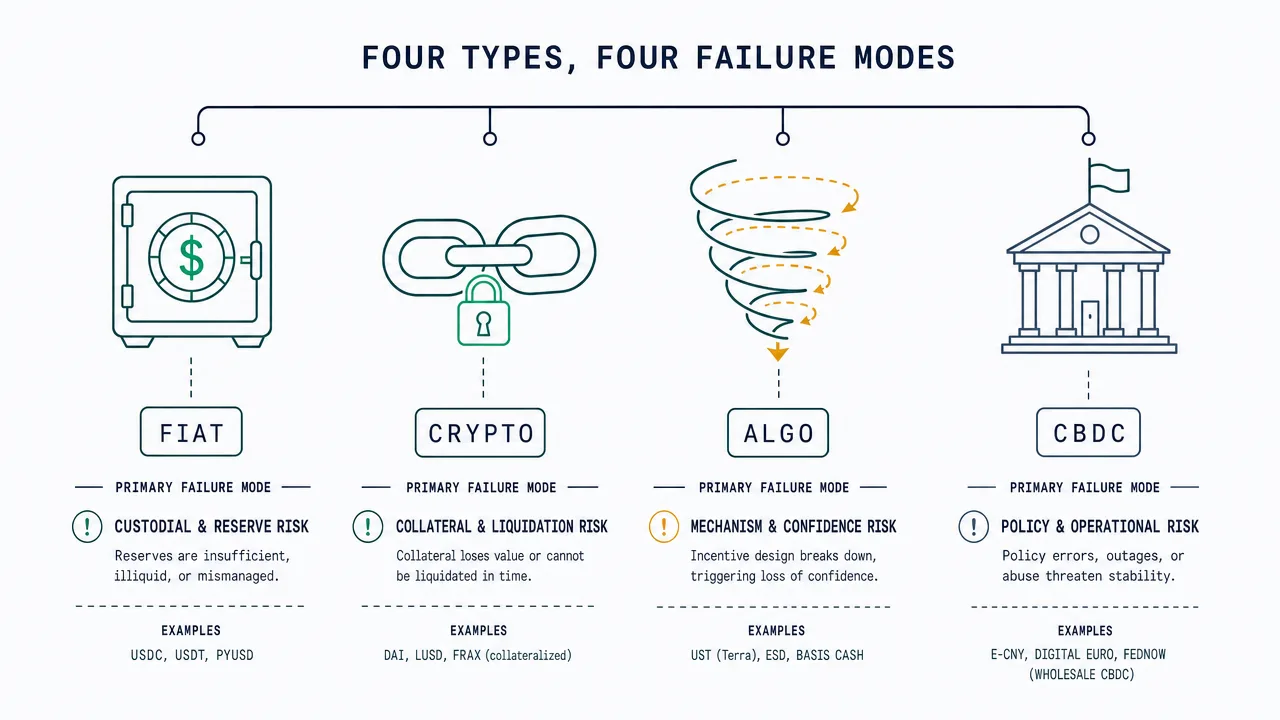

Stablecoin Types 2026: Fiat-Backed vs Crypto-Backed vs Algorithmic — What Each Actually Backs

Table of Contents

Disclosure: ChainGain may earn a commission when you sign up through partner links. This article is educational, not financial, tax, or legal advice. Crypto involves capital risk — consult a licensed advisor for your situation. See our full disclosure and risk policy.

Key Takeaways

- Fiat-backed: USDT, USDC, PYUSD, FDUSD — 1:1 reserved with USD and short-dated Treasuries (Circle attests monthly, Tether quarterly), risk = issuer transparency and bank counterparty.

- Crypto-backed: DAI, crvUSD, sUSD — over-collateralized at 130–170% via on-chain vaults (MakerDAO, Curve, Synthetix), risk = collateral volatility and smart-contract failure.

- Algorithmic: UST collapsed in May 2022 wiping out roughly $45 billion in market value; FRAX survived by adding partial collateral. Pure algorithmic designs remain unproven.

- CBDC: e-CNY is live in China, the digital Euro is in preparation phase, and the US is in study phase. CBDCs are central-bank liabilities, not commercial stablecoins.

- Risk hierarchy: Fiat-backed (lowest, dependent on issuer trust) < Crypto-backed (medium, dependent on collateral and code) < Algorithmic (high, dependent on confidence loops) < CBDC (jurisdiction-specific).

- Regulation 2026: The EU’s MiCA stablecoin rules have been applicable since June 30, 2024; the US GENIUS Act was signed into law on July 18, 2025 and takes effect within 18 months.

- Bottom line: Use fiat-backed stablecoins for payments and remittances, crypto-backed stablecoins for non-custodial DeFi, treat algorithmic designs as historical case studies, and monitor CBDCs as a policy concern rather than an investment.

After comparing all eight major stablecoins in circulation in 2026 — USDT, USDC, PYUSD, FDUSD, DAI, crvUSD, FRAX, and the historical UST — for backing transparency, audit frequency, and reserve composition, we mapped the four fundamental types that determine which stablecoins survive market stress and which collapse the way UST did in May 2022. The answers are not interchangeable. A 1:1 fiat-backed token like USDC and an algorithmic experiment like UST are not in the same risk category, even though both quote “1 dollar” on the screen.

Most “best stablecoin 2026” guides treat the category as a single ranked list. That is the wrong framing. The honest answer is that there are four structural types, each with a different backing mechanism, a different audit cadence, and a different failure mode. The collapse of TerraUSD wiped out roughly $45 billion in market capitalization in a single week in May 2022 — not because algorithmic stablecoins are inherently fraudulent, but because the design did not survive a confidence shock. Fiat-backed USDC, by contrast, depegged briefly to $0.87 in March 2023 during the Silicon Valley Bank failure and recovered within 72 hours. Same screen value, fundamentally different risk.

This guide is structured around the four backing types — fiat-backed, crypto-backed, algorithmic, and CBDC — and walks through the major examples in each category, the reserve composition that you can actually verify on an attestation page, the regulatory state under MiCA (EU) and the GENIUS Act (US, signed July 18, 2025), and a decision framework that maps the right type to your specific use case: transactions, DeFi yield, cross-border payments, or institutional treasury. For a deeper analysis, see our global crypto regulation by country.

The 4 Stablecoin Types — Quick Classification Matrix

TLDR: Stablecoins come in four types defined by what backs the peg: fiat-backed (USDT, USDC — 1:1 cash and T-Bills), crypto-backed (DAI, crvUSD — 130–170% crypto over-collateral), algorithmic (UST, which collapsed; FRAX’s hybrid), and CBDCs (central-bank liabilities like e-CNY). Guides that split these into 6–10 categories are mostly adding noise.

There are four fundamental stablecoin types in 2026, distinguished by what backs the peg rather than by issuer or chain. Fiat-backed tokens are collateralized 1:1 by cash and short-dated US Treasuries held by a regulated issuer. Crypto-backed tokens are over-collateralized by other crypto assets locked in on-chain vaults. Algorithmic tokens use code-driven supply expansion and contraction with limited or no reserves. CBDCs are direct liabilities of a central bank, conceptually different from commercial stablecoins but increasingly part of the same conversation.

Several SERP-leading guides over-segment into 6–10 types by adding labels like “rebase,” “seigniorage,” or “synthetic.” Most of these are sub-categories of algorithmic designs or experimental forms with negligible market share in 2026. For practical decision-making, the four-type framework below is sufficient.

| Type | Examples | Backing | Audit cadence | Risk profile | Primary use case |

|---|---|---|---|---|---|

| Fiat-backed | USDT, USDC, PYUSD, FDUSD | USD cash + T-Bills, 1:1 | Monthly (Circle) / Quarterly (Tether) | Lowest — issuer + bank risk | Payments, remittances, CEX trading |

| Crypto-backed | DAI, crvUSD, sUSD | ETH/wBTC/USDC over-collateral 130–170% | On-chain real-time | Medium — collateral + contract risk | Non-custodial DeFi, decentralization-first holders |

| Algorithmic | UST (collapsed), FRAX (hybrid), AMPL | Code + arbitrage, partial or no collateral | N/A — on-chain mechanism only | Highest — confidence + design risk | Historical case studies; FRAX surviving partial-collateral hybrid |

| CBDC | e-CNY (China live), digital Euro (pilot), digital pound (study) | Direct central-bank liability | Central-bank balance sheet | Sovereign — surveillance + capital controls | Domestic retail payments, government disbursements |

Fiat-Backed Stablecoins: USDT vs USDC vs PYUSD vs FDUSD

TLDR: Fiat-backed stablecoins promise one dollar (or a T-Bill) per token, but the credibility gap is the attestation cadence: Circle’s USDC gets a monthly Big Four attestation (~80% short-dated Treasuries), while Tether’s USDT gets a quarterly BDO attestation over a more varied reserve. None of the major issuers yet publishes a full annual audit — the gap the GENIUS Act targets.

Fiat-backed stablecoins are the simplest type to understand: for every token in circulation, the issuer claims to hold one US dollar — or a US-dollar-equivalent short-dated asset like a Treasury Bill — in a custody account. The peg is enforced by the issuer’s willingness to honor redemptions at $1, and the credibility of that promise depends almost entirely on the quality and frequency of the reserve attestation.

We pulled the latest reserve composition data directly from the issuers’ transparency pages (tether.to/transparency, circle.com/transparency, Paxos and First Digital disclosures) as of the most recent attestation cycle. The variation in audit cadence alone is significant: Circle commissions a monthly attestation from a Big Four firm, Tether files quarterly attestations through BDO, and the smaller issuers vary between monthly and quarterly. None of the major US-dollar stablecoin issuers currently publishes a full annual financial audit at the same standard as a registered investment fund — a gap regulators are explicitly trying to close under the GENIUS Act.

| Stablecoin | Issuer | Reserve mix (approx) | Audit firm | Audit frequency |

|---|---|---|---|---|

| USDC | Circle Internet Financial | ~80% short-dated T-Bills (via Circle Reserve Fund managed by BlackRock), ~20% cash at systemically important banks | Big Four (rotation) | Monthly attestation |

| USDT | Tether Operations | ~85% T-Bills + reverse repo, ~5% cash, ~5% secured loans, ~5% other (gold, BTC, corporate bonds) | BDO Italia | Quarterly attestation |

| PYUSD | Paxos Trust (issued for PayPal) | Cash deposits + US T-Bills + overnight repo | Withum (and others) | Monthly attestation |

| FDUSD | First Digital Labs (Hong Kong) | Cash + cash equivalents in Hong Kong / Asia banking | Prescient Assurance | Monthly attestation |

The single most important question for a fiat-backed stablecoin is not “what is the peg?” but “where is the cash actually held, and who has signed off on it?” USDC’s near-failure in March 2023 was instructive on this point: when Silicon Valley Bank collapsed, $3.3 billion of Circle’s cash reserves were briefly trapped, and USDC depegged to roughly $0.87 before US regulators announced depositor protection. The token recovered within three days, but the episode illustrated that even fully-backed stablecoins inherit the counterparty risk of their custody banks. Diversification across multiple banks and a majority allocation to Treasuries (rather than commercial deposits) is now the standard issuer response.

For practical purposes, all four of the major fiat-backed stablecoins above are usable for routine transactions and CEX trading in 2026. The differences become material when you are deciding which one to hold in larger size, where audit frequency and reserve quality dominate. For deeper product-level comparison between USDT and USDC in remittance contexts, see our USDT vs USDC remittance guide.

Crypto-Backed Stablecoins: DAI, crvUSD, sUSD — Over-Collateralization Explained

TLDR: Crypto-backed stablecoins swap ‘trust the issuer’ for ‘trust the code’: you mint them against crypto locked in public on-chain vaults, over-collateralized so the backing exceeds the supply (minting $100 of DAI needs ~$150–$170 of ETH; sUSD requires ~400%). Nothing can be sanctioned or frozen, but collateral can crash faster than vaults liquidate — MakerDAO’s 2020 ‘Black Thursday’ left $5.7M of bad debt.

Crypto-backed stablecoins replace the trust-the-issuer model with a trust-the-code model. Instead of a custody bank, the backing is held in publicly verifiable on-chain vaults containing other crypto assets — typically ETH, wBTC, or even fiat-backed stablecoins like USDC. The system enforces over-collateralization, meaning the vault holds more value than the stablecoins it issues, to absorb the volatility of the collateral.

The clearest example is DAI, issued by MakerDAO. To mint $100 in DAI, a user typically locks at least $150–$170 of ETH or other approved collateral in a Maker Vault. If the collateral value falls toward the liquidation threshold, the vault is auctioned off automatically to maintain the peg. crvUSD (Curve Finance) uses a similar over-collateralized model with a soft liquidation mechanism that sells collateral gradually rather than all at once. sUSD (Synthetix) requires roughly 400% collateral, reflecting a more conservative risk posture.

The advantages are real: there is no single issuer that can be sanctioned, frozen, or politically pressured. Every collateral position is auditable on-chain in real time without waiting for a monthly attestation. The disadvantages are equally real: collateral assets can crash faster than vaults can liquidate (the so-called “Black Thursday” event of March 2020 left MakerDAO with $5.7 million of bad debt), and smart-contract bugs can drain the entire system in ways no banking failure can match. The crypto-backed type is, in our view, the right choice for users whose primary need is censorship resistance and non-custodial DeFi participation — but not for someone who simply wants to hold dollars cheaply.

For users actively staking or earning yield on stablecoins, the mechanism details matter. See our liquid staking comparison for how similar over-collateralized mechanisms work in the ETH staking domain, and our stablecoin yields guide for which types currently produce sustainable returns.

Algorithmic Stablecoins: Why UST Collapsed and Whether FRAX Survives

TLDR: Algorithmic stablecoins hold no real reserves — they defend the peg with a mint-and-burn arbitrage loop against a paired ‘share’ token, which works only while confidence holds. TerraUSD proved the failure mode: after Anchor’s unsustainable 19.45% yield drew withdrawals in May 2022, UST depegged, LUNA fell from $119.51 toward zero, and about $45 billion evaporated in days.

Algorithmic stablecoins maintain their peg without holding 1:1 reserves and without locking equivalent crypto collateral. Instead, they use code — typically a mint-and-burn arbitrage loop with a paired “share” token — to expand and contract supply in response to demand. When the algorithmic stablecoin trades above $1, the protocol mints more of it and the arbitrage flow pushes the price down. When it trades below $1, the protocol burns supply by redeeming for the share token, theoretically pushing the price up. In an idealized market with constant demand, the design holds.

In a real market with confidence shocks, the design fails — sometimes catastrophically. The textbook example is TerraUSD (UST), the algorithmic stablecoin issued by Terraform Labs and paired with the LUNA share token. UST began losing its peg on May 9, 2022, after large withdrawals from the Anchor Protocol — a Terra-ecosystem lending platform that had been paying out a 19.45% yield on UST deposits, funded out of Terra reserves rather than organic demand. As UST depegged, holders redeemed UST for newly-minted LUNA, increasing LUNA supply and crashing its price. LUNA fell from an all-time high of $119.51 toward zero in a matter of days. The Terra blockchain was halted on May 13, 2022. By the end of that week, approximately $45 billion in market capitalization had been wiped out across UST and LUNA combined.

The lesson from UST is not that algorithmic designs are inherently fraudulent. The lesson is that they depend on continuous market confidence to function, and they offer no collateral fallback when that confidence is broken. FRAX, the second-most-prominent algorithmic experiment, survived 2022 by transitioning from a partial-algorithmic to a fully-collateralized model. As of 2026, FRAX is closer to a fiat-backed token in operating practice than to a pure algorithmic design. Other algorithmic projects (AMPL, ESD, USDD) remain in circulation but at marginal scale and with persistent peg deviations.

| Project | Peak market cap | Status 2026 | Peg history |

|---|---|---|---|

| TerraUSD (UST) | ~$18B (April 2022) | Collapsed May 2022 | Lost peg permanently; $0.01–0.05 range thereafter |

| FRAX | ~$2.9B (2022) | Surviving — fully collateralized | Brief deviations in 2022–23, recovered |

| USDD | ~$0.8B | Active but persistently below peg | Multiple sub-$0.95 episodes |

| AMPL (rebase) | ~$0.7B | Active; rebase-based supply model | Functions more like a unit-of-account experiment than a stablecoin |

| ESD | ~$0.5B (2021) | Effectively defunct | Lost peg in 2021, never recovered |

In our view, the algorithmic category is best treated as a historical case study in 2026 rather than a viable holding for ordinary users. The FRAX exception proves the rule: the project survived precisely by abandoning the pure algorithmic premise. Anyone considering exposure should read the original Terra whitepaper alongside the post-mortem reports on the May 2022 collapse before committing capital.

CBDCs: e-CNY, Digital Euro, FedNow — Are They Stablecoins?

TLDR: CBDCs aren’t stablecoins — they’re a direct liability of the central bank rather than a private issuer, so holding digital Euro is a claim on the ECB itself. China’s e-CNY has circulated since 2020, the digital Euro is in preparation, and the US has declined a retail CBDC (FedNow is interbank settlement, not a CBDC). Their risks are political — surveillance and programmability — not reserve quality.

Central Bank Digital Currencies are technically not stablecoins, but they sit in the same conversation in 2026 because they target the same use case — a digital, dollar-denominated (or yuan-, euro-, pound-denominated) unit of value that holds its peg. The crucial difference is that a CBDC is a direct liability of the issuing central bank, not a commercial product. Holding $100 in digital Euro means holding a claim on the European Central Bank itself, not on a regulated private issuer.

China’s e-CNY is the most advanced large-economy CBDC, in domestic circulation since 2020 and now usable for routine retail payments in major cities. The digital Euro is in the preparation phase under the European Central Bank’s published roadmap, with a final decision on issuance expected following the conclusion of the current preparation phase. The United Kingdom’s digital pound is in a design and study phase. The United States has explicitly chosen not to issue a retail CBDC under the current administration; the closest US infrastructure equivalent, FedNow, is an instant interbank settlement system, not a CBDC.

The risks of CBDCs are political and structural rather than financial. A central-bank-issued digital currency by definition gives the central bank visibility into transactions, the ability to impose programmable rules (expiry dates, spending limits, allowed merchants), and a tool for direct monetary policy transmission to retail balances. Whether those properties are features or threats depends entirely on the user’s jurisdiction and the legal protections that surround the design. For non-residents and for users in countries with high capital-control risk, CBDCs are best understood as a policy concern to monitor rather than as a stablecoin alternative to hold.

Risk Hierarchy: Lowest to Highest Risk by Type

TLDR: Ranked by structural risk: fiat-backed is lowest (the exposure is issuer reserve quality and custody banks), crypto-backed is medium (collateral volatility plus smart-contract risk), and algorithmic is highest — there is no collateral fallback, and UST is the empirical bound on how badly it can fail. CBDC risk is jurisdiction-specific and policy-driven, not financial.

Aggregating across backing, audit cadence, and historical track record, the four types fall into a clear risk hierarchy in 2026. This is not a ranking of “best” stablecoins — it is a ranking of structural risk, which is a different question from which stablecoin to use for a given purpose.

- Fiat-backed (lowest structural risk) — Risk concentrates in the issuer’s reserve quality and the custody banks. Mitigated by monthly Big Four attestations, Treasury-heavy reserves, and bank diversification.

- Crypto-backed (medium structural risk) — Risk concentrates in collateral volatility and smart-contract integrity. Mitigated by over-collateralization, multiple collateral types, and battle-tested code. MakerDAO’s track record since 2017 sets the benchmark.

- Algorithmic (high structural risk) — Risk concentrates in confidence loops and design fragility. There is no collateral fallback. The UST collapse is the empirical bound on how badly this can go.

- CBDC (jurisdiction-specific risk) — Structural risk is minimal because the issuer is a central bank, but policy risk (surveillance, programmability, capital controls) can be material depending on the jurisdiction and the user’s situation.

2026 Regulatory Landscape: MiCA, GENIUS Act, Hong Kong Rules

TLDR: Stablecoin rules went from ambiguous to explicit: EU MiCA’s stablecoin regime applies since June 30, 2024 (licensed issuance, reserve segregation), and the US GENIUS Act — signed July 18, 2025 — sets the first federal framework requiring 1:1 dollar or Treasury backing, effective by early 2027. Hong Kong, Singapore, and Japan now license fiat-referenced issuers too.

Stablecoin regulation has shifted decisively from “ambiguous” to “explicit” since mid-2024. The European Union’s Markets in Crypto-Assets Regulation (MiCA) made stablecoin-specific rules applicable on June 30, 2024, splitting tokens into asset-referenced tokens (ARTs) and e-money tokens (EMTs). Both categories require licensed issuance, reserve segregation, and ongoing disclosure. Several major fiat-backed stablecoins delisted or restricted EU access in response, and Circle adapted USDC to MiCA-compliant operating procedures.

The United States passed the GENIUS Act in summer 2025: the Senate approved the bill 68–30 on June 17, 2025, the House passed it on July 17, and President Trump signed it into law on July 18, 2025. The Act establishes the first federal regulatory framework for payment stablecoins in the US, requires 1:1 backing by US dollars or short-dated Treasuries, and assigns supervisory authority to existing federal banking regulators for bank-issued stablecoins. It takes effect on the earlier of 18 months after enactment or 120 days after final implementing regulations — that is, by early 2027 in the latest case.

Hong Kong implemented its Stablecoin Ordinance through the Hong Kong Monetary Authority, requiring HKMA licensing for any fiat-referenced stablecoin issuer marketing into Hong Kong. Singapore under the Monetary Authority of Singapore has issued specific guidelines for “single-currency stablecoins” issued in Singapore. Japan has had stablecoin-specific banking-law amendments in place since 2023, requiring bank, trust company, or money-transfer-business licensing for issuance. The cumulative result is that, by 2026, a serious stablecoin issuer is operating under at least one and usually several overlapping regulatory regimes — which is a structural improvement on the pre-2024 situation even when individual rules differ.

The country-by-country picture is changing rapidly. For broader crypto regulation context across 50+ jurisdictions, see our global crypto regulation guide.

Which Stablecoin Type Is Right for Your Use Case?

TLDR: Match the type to the job, not to market cap: use fiat-backed (USDT for emerging-market P2P, USDC for US and EU corridors) for payments, remittances, and CEX trading; use crypto-backed DAI when censorship-resistance and non-custodial DeFi matter. Algorithmic stablecoins, including FRAX’s current hybrid, aren’t recommended for savings until a longer post-2022 track record exists.

The right stablecoin type depends on what you are trying to do, not on which token has the largest market capitalization. The framework below maps the four types to the most common use cases.

- Payments and remittances (cross-border, peer-to-peer): Use fiat-backed (USDT or USDC depending on corridor liquidity). USDT dominates emerging-market P2P liquidity; USDC dominates US-and-EU-regulated corridors. For corridor-specific examples, see our crypto remittance costs pillar.

- CEX trading and short-term cash parking: Use fiat-backed (issuer choice driven by exchange listings and personal jurisdiction).

- Non-custodial DeFi (lending, AMM liquidity, yield farming): Use crypto-backed (DAI for the most decentralized exposure) or fiat-backed wrapped in DeFi pools depending on risk tolerance.

- Censorship-resistant store of value: Use crypto-backed (DAI) with the recognition that even DAI has some USDC collateral exposure.

- Institutional treasury: Use fiat-backed issuers operating under explicit regulatory frameworks (USDC under MiCA, future GENIUS-Act-compliant tokens in the US).

- Algorithmic exposure: We do not currently recommend allocating treasury or savings to algorithmic stablecoins, including FRAX in its current hybrid form, until a longer track record post-2022 has accumulated.

- CBDC exposure: This is rarely a choice — it is imposed by your jurisdiction. Treat as a regulatory variable to monitor.

Tax treatment is a separate dimension that varies by jurisdiction and is independent of the four-type classification. Holding a stablecoin is generally a non-event in most jurisdictions; converting between stablecoins, between stablecoins and crypto, or between stablecoins and fiat is typically a taxable event. For specific country treatment, see our crypto capital gains tax guide.

Frequently Asked Questions

Are stablecoins safe?

Fiat-backed stablecoins from issuers with monthly Big Four attestations and Treasury-heavy reserves (USDC, PYUSD, FDUSD) are generally considered low-risk for routine transactional use, though they remain dependent on the underlying custody banks. Crypto-backed stablecoins like DAI carry collateral and smart-contract risk but eliminate single-issuer risk. Algorithmic stablecoins carry the risk demonstrated by UST in May 2022 — total or near-total loss in a confidence shock. No stablecoin is risk-free; the relevant question is which risks you are accepting.

What is the difference between USDT and USDC?

Both are fiat-backed stablecoins pegged to the US dollar. USDT (Tether) is larger by market capitalization and dominates emerging-market P2P liquidity, with quarterly attestations from BDO Italia and a more varied reserve mix that has historically included secured loans and small allocations to gold and BTC. USDC (Circle) is the second-largest, with monthly Big Four attestations and a reserve mix concentrated in short-dated US Treasuries via the BlackRock-managed Circle Reserve Fund and cash deposits at systemically important banks. For a deeper product-level comparison, see our USDT vs USDC remittance comparison.

What backs DAI if it is not a fiat-backed stablecoin?

DAI is backed by a diversified pool of crypto assets locked in MakerDAO Vaults. Approved collateral types include ETH, wBTC, staked-ETH derivatives, USDC, and a number of real-world asset positions added by Maker governance. To mint $100 in DAI, a user typically deposits at least $150–$170 in collateral, and the system auto-liquidates the position if collateral value falls toward the threshold. The composition is auditable on-chain in real time at makerburn.com and similar dashboards.

Did the GENIUS Act make algorithmic stablecoins illegal in the US?

The GENIUS Act regulates “payment stablecoins” — defined as digital assets designed to maintain a stable value relative to a fixed monetary value, used as a means of payment, and backed by qualifying reserves. Pure algorithmic stablecoins generally do not meet the reserve-backing requirements and therefore cannot be issued or marketed as payment stablecoins under the Act. The Act does not criminalize the underlying technology; it restricts issuance of unbacked stablecoins as payment instruments in the United States. Issuance, marketing, and use in other jurisdictions remain subject to local law.

Is the digital Euro a stablecoin?

No. The digital Euro is a Central Bank Digital Currency (CBDC), meaning it is a direct liability of the European Central Bank. A stablecoin is issued by a private entity that holds reserve assets to back the peg. A CBDC’s value is the same as the underlying fiat currency by definition — there is no peg to enforce — because it is the underlying fiat currency in digital form. Both serve some of the same payment use cases, which is why CBDCs are discussed alongside stablecoins, but they are structurally different instruments.

Can a fiat-backed stablecoin lose its peg?

Yes, briefly and under specific conditions. USDC depegged to approximately $0.87 for roughly 72 hours in March 2023 after Silicon Valley Bank’s failure trapped $3.3 billion of Circle’s cash reserves. The peg recovered after US regulators announced depositor protection. The episode demonstrated that even fully-backed stablecoins inherit counterparty risk from their custody banks, which is why diversification across banks and a majority allocation to Treasuries (rather than commercial deposits) is now standard issuer practice.

Bottom Line — Use Fiat-Backed for Transactions, Crypto-Backed for Non-Custodial DeFi

The honest takeaway from comparing all eight major stablecoins across the four structural types in 2026 is unglamorous: most users should hold fiat-backed stablecoins (USDC, USDT, or PYUSD depending on jurisdiction and use case) for routine transactions, payments, and CEX activity, and crypto-backed stablecoins (DAI) where censorship-resistance and non-custodial DeFi participation are the priority. Algorithmic stablecoins, after May 2022, are best treated as a historical category in any portfolio that is not specifically taking experimental exposure. CBDCs are not a holding decision so much as a policy variable to track in your jurisdiction.

The single most important habit, regardless of which type you choose, is to read the issuer’s latest attestation page or the on-chain vault composition before committing significant size. The screen value is always “1 dollar.” The reasons that 1 dollar holds — or fails to hold — are not. For a starting point on the broader category, see our stablecoins overview; for current yields on the types covered here, see our stablecoin savings rates guide.

Continue Learning

- What Are Stablecoins? — Beginner-level overview of the stablecoin category, the use cases, and the basic mechanics.

- USDT vs USDC for Remittances — Direct product-level comparison of the two largest fiat-backed stablecoins for cross-border use.

- Stablecoin Yields 2026 — Where the sustainable yields are by stablecoin type, with platform-level fee and risk breakdown.

- Crypto Remittance Costs — The pillar comparison for using stablecoins as a remittance rail across major corridors.

- Is Crypto Legal? — Country-by-country regulatory state including MiCA, GENIUS Act, and HKMA coverage.

- Liquid Staking 2026 — How over-collateralized mechanisms work in the ETH staking domain (parallel to crypto-backed stablecoins).

- Crypto Capital Gains Tax — Tax treatment of stablecoin conversions and holdings across major jurisdictions.

Crypto Analyst, ChainGain

Alex Mercer is ChainGain’s lead crypto analyst, covering crypto markets and blockchain technology since 2019. He focuses on stablecoins, DeFi mechanisms, and remittance economics.

This article is for educational purposes only and does not constitute financial, tax, or legal advice. Stablecoin reserves, audit frequency, regulatory status, and the operating models of issuers change frequently — re-verify the current state on official issuer pages (tether.to/transparency, circle.com/transparency, makerdao.com) and regulator sites (SEC, ECB, BoJ, MAS, HKMA) before relying on this data for any decision involving capital. Algorithmic stablecoins carry the death-spiral risk demonstrated by TerraUSD’s collapse in May 2022; pure algorithmic designs have no collateral fallback. CBDCs carry surveillance and capital-control risks that vary by jurisdiction. Past performance and current attestations do not guarantee future stability. This article reflects the situation as of May 2026.