What Are Stablecoins? USDT, USDC, DAI Explained Simply (2026)

Table of Contents

Beginner

A stablecoin is a type of cryptocurrency designed to maintain a stable value, usually pegged 1:1 to a fiat currency like the US dollar. While Bitcoin and Ethereum can swing 10% in a day, stablecoins stay at approximately $1.00 — making them the bridge between traditional finance and the crypto world.

Stablecoins are the most practical part of cryptocurrency that most people overlook. I use them daily — to park profits during volatile markets, send money internationally in minutes instead of days, and access DeFi yields that traditional savings accounts can’t match. In countries like Nigeria, Brazil, and Pakistan, stablecoins have become a genuine financial tool for millions of people fighting currency devaluation.

This guide explains what stablecoins are, how they maintain their peg, the different types available, and the real risks you should know about.

What Are Stablecoins? A Clear Definition

A stablecoin is a cryptocurrency whose value is pegged to a stable reference asset — typically the US dollar, though some track the euro, gold, or other currencies. The goal is simple: combine the speed and accessibility of crypto with the price stability of traditional money.

When you hold 100 USDT (Tether) or 100 USDC (USD Coin), you hold the crypto equivalent of $100. The value doesn’t fluctuate like Bitcoin. This makes stablecoins useful for:

- Trading — Move in and out of volatile crypto positions without converting back to bank currency

- Payments — Send dollars anywhere in the world in minutes, 24/7, for pennies

- Savings — Hold dollar value without a US bank account (critical in countries with unstable currencies)

- DeFi — Earn yield by lending stablecoins through decentralized protocols

As of early 2026, the total stablecoin market capitalization exceeds $200 billion, with Tether (USDT) and USD Coin (USDC) accounting for over 85% of that value. According to Chainalysis data, stablecoins now represent over 50% of all on-chain transaction volume — more than Bitcoin and Ethereum combined.

How Do Stablecoins Maintain Their Peg?

The central question with any stablecoin is: how does it stay at $1? Different stablecoins use different mechanisms, and understanding these is crucial because they directly affect the coin’s risk profile.

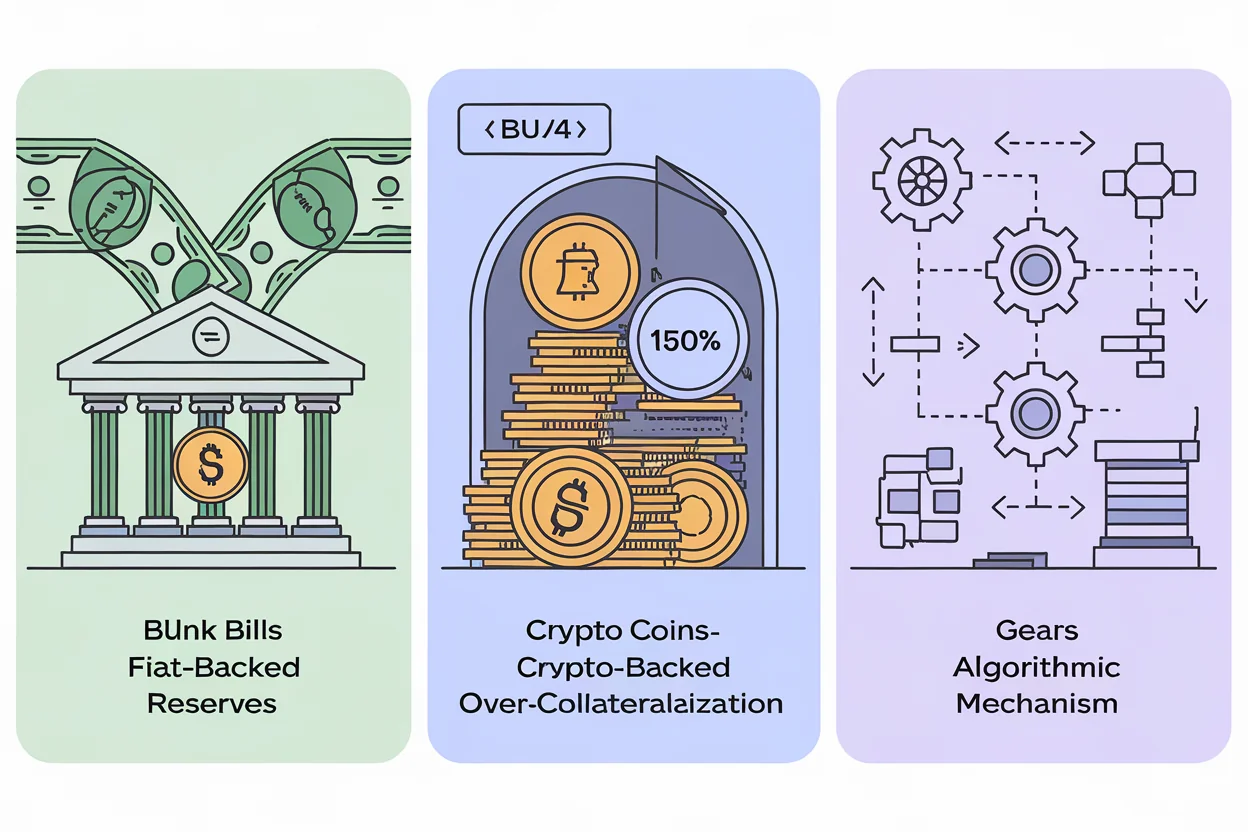

Fiat-Backed (Reserve-Based)

The simplest model. For every stablecoin issued, the company holds an equivalent amount of real-world assets in reserve. When you buy 1 USDT, Tether Limited holds $1 (or equivalent) in a bank account or in short-term US Treasury bills.

How the peg holds: If 1 USDT trades below $1 on exchanges, arbitrage traders buy it cheaply and redeem it directly from Tether for $1 — pocketing the difference. This buying pressure pushes the price back up. The reverse happens if it trades above $1.

Trust requirement: You must trust that the issuing company actually holds sufficient reserves. This has been a point of controversy, particularly with Tether, which faced regulatory scrutiny over the composition of its reserves.

Examples: USDT (Tether), USDC (Circle), FDUSD (First Digital)

Crypto-Backed (Over-Collateralized)

Instead of holding dollars in a bank, these stablecoins are backed by cryptocurrency locked in smart contracts — typically with more collateral than the stablecoin is worth (over-collateralized) to absorb price fluctuations in the underlying crypto.

How it works: To mint 100 DAI, you might need to lock $150 worth of ETH as collateral (150% collateralization ratio). If ETH’s price drops and your collateral falls below the minimum ratio, the system automatically liquidates your position to maintain DAI’s peg.

Trust requirement: You trust the smart contract code and the governance system, rather than a company. The code is open-source and auditable.

Examples: DAI (MakerDAO), LUSD (Liquity)

Algorithmic

Algorithmic stablecoins use automated supply adjustments — minting new coins when the price rises above $1 and burning coins when it drops below — to maintain their peg without holding reserves.

The critical warning: This model carries the highest risk. The most infamous example is TerraUSD (UST), which lost its peg catastrophically in May 2022, collapsing from $1 to near $0 and wiping out approximately $40 billion in value. The event triggered a broader crypto market crash and led to criminal charges against its creators.

Examples: FRAX (partially algorithmic), former UST (failed)

Major Stablecoins Compared

| Stablecoin | Symbol | Type | Market Cap (2026) | Reserves | Transparency |

|---|---|---|---|---|---|

| Tether | USDT | Fiat-backed | ~$140B | US T-bills, cash, loans | Quarterly attestations |

| USD Coin | USDC | Fiat-backed | ~$55B | US T-bills, cash deposits | Monthly audits by Deloitte |

| DAI | DAI | Crypto-backed | ~$5B | ETH, USDC, RWAs in smart contracts | On-chain, fully verifiable |

| First Digital USD | FDUSD | Fiat-backed | ~$3B | Cash, T-bills | Monthly attestations |

| FRAX | FRAX | Hybrid | ~$1B | Partial reserves + algorithmic | On-chain + attestations |

| Euro Coin | EURC | Fiat-backed | ~$456M | EUR reserves (MiCA-compliant) | Monthly audits |

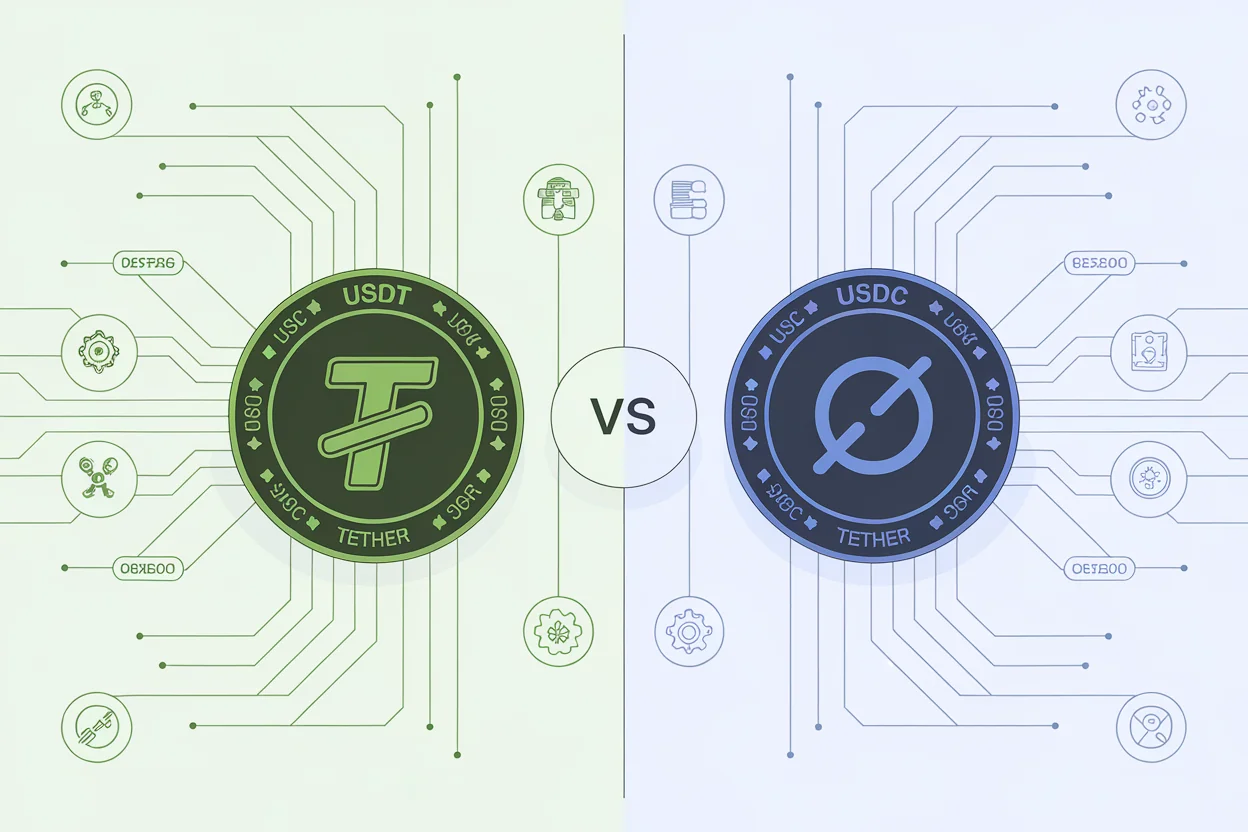

USDT vs. USDC: The Two Giants

Most people choosing a stablecoin will pick between USDT and USDC. Here’s how they compare:

| Factor | USDT (Tether) | USDC (Circle) |

|---|---|---|

| Market dominance | #1 (~70% of stablecoin market) | #2 (~25% of stablecoin market) |

| Liquidity | Highest — available on virtually every exchange | High — widespread but less than USDT |

| Transparency | Quarterly attestations (criticized as insufficient) | Monthly audits by major accounting firm |

| Regulation | Based in British Virgin Islands | US-regulated, compliant with MiCA (EU) |

| Supported chains | Ethereum, Tron, Solana, BSC, + many more | Ethereum, Solana, Base, Avalanche, + others |

| Best for | Maximum liquidity, emerging market access | Institutional use, regulatory compliance |

In my experience, USDT has better availability in emerging markets (Africa, Southeast Asia, CIS), while USDC is preferred by institutions and in regulated environments. For everyday use, the practical difference is minimal — but for large holdings, USDC’s stronger transparency gives me more confidence.

Real-World Uses of Stablecoins

Stablecoins aren’t just a crypto trader’s tool. They’re solving real financial problems for real people.

International Remittances

Sending $200 from the US to Nigeria through traditional channels (Western Union, bank wire) costs $10-$25 in fees and takes 1-5 days. Sending $200 in USDT on the Tron network costs less than $1 and arrives in under a minute.

According to World Bank data, global remittance flows exceeded $656 billion in 2025. The average fee was 6.2%. Stablecoins are cutting that dramatically — particularly on corridors to Sub-Saharan Africa, South Asia, and Latin America.

Inflation Hedge in Emerging Markets

In countries experiencing high inflation or currency instability (Argentina, Nigeria, Turkey, Pakistan, Indonesia, Ukraine), holding savings in USDT or USDC effectively dollarizes your savings without needing a US bank account. Vietnam (#4 in global crypto adoption), Indonesia (#7), and Ukraine (#8, #1 population-adjusted) have seen explosive stablecoin growth driven by this need.

I’ve corresponded with traders in Lagos, Istanbul, Jakarta, and São Paulo who keep the majority of their savings in stablecoins, converting to local currency only when they need to spend. For them, stablecoins aren’t speculative — they’re a financial necessity.

DeFi Yield

Stablecoins can be lent through decentralized protocols to earn interest. As of early 2026, lending USDC on major protocols yields 4-8% APY — comparable to or better than many traditional savings accounts, and significantly higher than rates in most emerging economies.

Important caveat: DeFi yields carry smart contract risk, platform risk, and regulatory risk. They are not equivalent to insured bank deposits. Only use reputable, audited protocols, and never put in more than you can afford to lose.

E-Commerce and Payments

A growing number of merchants accept stablecoins, particularly in crypto-native industries. Freelancers in the global gig economy increasingly receive payment in USDT or USDC, avoiding the delays and fees of international bank transfers.

Stablecoin Risks You Should Know

Stablecoins are more stable than other crypto, but they are not risk-free. Understanding these risks is essential before holding significant amounts.

De-Pegging Risk

A stablecoin can lose its $1 peg. This has happened multiple times:

- UST (2022) — Complete collapse from $1 to ~$0. $40 billion destroyed. Algorithmic model failed.

- USDC (March 2023) — Temporarily dropped to $0.87 when Silicon Valley Bank (which held $3.3B of USDC reserves) failed. Recovered within days after the US government backstopped SVB depositors.

- USDT (multiple) — Brief dips to $0.95-$0.98 during high-stress market events. Always recovered.

The lesson: fiat-backed stablecoins from major issuers have always recovered from temporary de-pegs. Algorithmic stablecoins have proven fragile under stress.

Regulatory Risk

Governments worldwide are developing stablecoin regulations. The EU’s MiCA regulation (Markets in Crypto-Assets) went into effect in 2024, with the final CASP authorization deadline on July 1, 2026. Under MiCA Title III, stablecoins are classified as either EMT (E-Money Tokens, single-fiat pegged like EURC) or ART (Asset-Referenced Tokens, multi-asset backed). Significant stablecoins must maintain 60%+ reserves in weekly liquid instruments and face direct EBA supervision. USDT availability in the EU may be restricted — EU residents should consider MiCA-compliant alternatives like EURC (Circle’s euro stablecoin, ~$456M market cap) or USDC. Japan has passed separate stablecoin-specific legislation under its revised Payment Services Act, making it one of the few countries with dedicated stablecoin law. The US has been debating stablecoin legislation since 2023.

Regulatory changes could affect: which stablecoins are available on exchanges, reserve requirements for issuers, and whether certain stablecoins are classified as securities.

Counterparty Risk

For fiat-backed stablecoins, you’re trusting the issuing company to:

- Actually hold the reserves they claim

- Manage those reserves responsibly (not investing in risky assets)

- Honor redemptions at par ($1)

- Remain solvent and operational

USDC’s monthly audits from Deloitte provide stronger assurance than Tether’s quarterly attestations, but neither is equivalent to FDIC insurance.

Smart Contract Risk (Crypto-Backed)

For stablecoins like DAI that rely on smart contracts, bugs or exploits in the code could theoretically compromise the system. While major protocols have undergone extensive audits, no smart contract is provably bug-free.

Censorship and Freezing

Both USDT and USDC issuers have the ability to freeze specific addresses on their contracts. This has been done in response to law enforcement requests and sanctions compliance. While this is rare for regular users, it means centralized stablecoins are not truly censorship-resistant.

Which Stablecoin Should You Use?

| Your Situation | Recommended Stablecoin | Why |

|---|---|---|

| Trading on exchanges | USDT | Most trading pairs, highest liquidity |

| Savings / large holdings | USDC | Better transparency, stronger regulatory position |

| DeFi on Ethereum | USDC or DAI | Wide DeFi support, DAI is decentralized |

| Sending money to emerging markets | USDT on Tron | Lowest fees, widest P2P availability |

| Maximum decentralization | DAI or LUSD | No central issuer can freeze your funds |

| EU/regulated environment | USDC | MiCA compliant |

| EU residents (MiCA zone) | EURC | Euro-denominated, MiCA-compliant, no EUR/USD FX risk |

How to Buy and Store Stablecoins

Getting stablecoins is straightforward:

- On a centralized exchange — Buy USDT or USDC using your local currency through any major exchange (Binance, Coinbase, Kraken). This is the simplest method for beginners.

- P2P trading — Buy directly from other users through platforms like Binance P2P. Popular in regions where exchange banking is limited.

- Swap from other crypto — Use a DEX or exchange to convert Bitcoin/ETH to USDT/USDC.

- Receive as payment — Share your wallet address to receive stablecoins from others.

Storage: Stablecoins are stored in the same wallets as other cryptocurrency. For significant amounts, use a hardware wallet. For daily use, a mobile wallet works well. The same security practices apply — protect your seed phrase and use reputable wallets.

Stablecoins and Blockchain Networks

The same stablecoin (e.g., USDT) exists on multiple blockchain networks, and the network you choose matters for transaction speed and fees:

| Network | Transaction Fee | Speed | Best For |

|---|---|---|---|

| Tron (TRC-20) | ~$1 | ~3 seconds | Cheap transfers, P2P, remittances |

| Ethereum (ERC-20) | $1-$10+ | ~15 seconds | DeFi, large institutional transfers |

| Solana (SPL) | < $0.01 | ~0.4 seconds | Ultra-cheap, fast payments |

| BNB Smart Chain (BEP-20) | ~$0.10 | ~3 seconds | Binance ecosystem users |

| Arbitrum / Optimism | $0.01-$0.10 | ~2 seconds | Ethereum DeFi with lower fees |

Critical reminder: Always verify you’re sending to an address on the correct network. Sending USDT on Tron to an Ethereum address (or vice versa) will result in permanent loss of funds.

Continue Learning

- What Is Cryptocurrency?

- How Blockchain Works

- How to Choose a Crypto Wallet

- Cryptocurrency Security

- Crypto vs Bank Transfers: Remittance Cost Guide

- Stablecoin Savings Guide: Protect Your Money from Inflation

- What Is DeFi? Decentralized Finance Explained

- Crypto Glossary: 200+ Terms Explained

- How to Spot and Avoid Crypto Scams

- How to Buy Your First Cryptocurrency

Frequently Asked Questions

Are stablecoins safe?

Major fiat-backed stablecoins (USDT, USDC) have maintained their dollar peg through multiple market crises and are generally considered safe for their intended purpose. However, they carry counterparty risk (you trust the issuer), regulatory risk, and are not FDIC insured. Algorithmic stablecoins carry significantly higher risk — the UST collapse in 2022 demonstrated they can fail catastrophically. For savings, stick to USDT or USDC from reputable platforms.

Can I earn interest on stablecoins?

Yes. You can earn yield on stablecoins through DeFi lending protocols (Aave, Compound), centralized lending platforms, or exchange savings products. As of 2026, rates typically range from 4-8% APY for major stablecoins. However, these yields carry risk — including smart contract bugs, platform insolvency, and regulatory changes. They are not equivalent to insured bank deposits. Only lend on reputable, audited protocols.

What is the difference between USDT and USDC?

Both are dollar-pegged fiat-backed stablecoins, but they differ in transparency and regulation. USDC (by Circle) publishes monthly audits and is regulated in the US. USDT (by Tether) provides quarterly attestations and is based in the British Virgin Islands. USDT has higher liquidity and wider availability, especially in emerging markets. USDC is preferred for institutional use and in regulated environments. For most retail users, either works well.

Can stablecoins lose their value?

Yes, though it’s rare for major stablecoins. Fiat-backed stablecoins like USDT and USDC have experienced brief de-pegs (dropping a few cents below $1) during extreme market stress but have always recovered. Algorithmic stablecoins like TerraUSD (UST) can collapse entirely — UST went from $1 to near $0 in May 2022. The safest approach is to use established fiat-backed stablecoins and avoid purely algorithmic ones.

Do I need to pay taxes on stablecoins?

In most jurisdictions, simply holding stablecoins is not a taxable event. However, earning yield on stablecoins (through lending or staking) is typically taxable as income. Selling stablecoins for fiat may also trigger a reporting obligation in some countries, even if there’s no capital gain. Tax treatment of crypto varies significantly by country — consult a tax professional for guidance specific to your jurisdiction.

Summary

Stablecoins are the most practical and widely-used category of cryptocurrency, combining the speed and accessibility of crypto with the stability of the US dollar. They’ve moved beyond trading tools to become essential financial infrastructure for remittances, savings, and payments worldwide.

Key takeaways:

- Stablecoins maintain a $1 peg through reserves (USDT, USDC), crypto collateral (DAI), or algorithms (risky)

- USDT offers maximum liquidity; USDC offers better transparency — both are suitable for most users

- Choose your blockchain network carefully — Tron and Solana are cheapest for transfers, Ethereum for DeFi

- Stablecoins carry real risks: de-pegging, counterparty risk, regulatory changes, and smart contract bugs

- Always verify the network before sending, and store significant amounts in a hardware wallet

Stablecoins aren’t perfect. They’re not insured, they carry counterparty risk, and the regulatory landscape is evolving. But for anyone needing dollar-denominated digital money — whether for trading, saving, or sending — they are currently the best tool available in crypto.

Continue Learning

- What Is Cryptocurrency? Complete Beginner’s Guide 2026

- How Blockchain Technology Works — Explained Simply

- How to Choose a Crypto Wallet: Complete Guide 2026

- Cryptocurrency Security: How to Protect Your Digital Assets

- Crypto vs Bank Transfers: The Real Cost of Sending Money Abroad in 2026

- Stablecoin Savings Guide: How to Protect Your Money from Inflation (2026)

- P2P Crypto Trading Safety Guide: How to Buy and Sell Safely

- Freelancer Crypto Payment Guide: Get Paid Globally, Spend Locally

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Stablecoins carry risks including de-pegging, counterparty failure, and regulatory changes. They are not FDIC insured or equivalent to bank deposits. Always do your own research before making financial decisions.

The Complete Stablecoins Guide Series

Everything in our stablecoins cluster, in one place:

- Earn 5-12% APY on Stablecoins: Best Platforms Compared (2026)

- Stablecoin Remittances Explained: How USDT/USDC Replace Wire Transfers (2026)

- Best Stablecoin Savings Rates 2026 (USDT & USDC)

- USDT vs USDC: Which Stablecoin Is Best for Remittances? (2026)

- Stablecoin vs Bitcoin: Which Is Better for Sending Money Abroad? (2026)

- Centralized Stablecoins 2026: USDT vs USDC vs DAI vs USDS Risk Comparison

- Best Stablecoin for Sending Money Abroad: 2026 Comparison (USDT vs USDC vs DAI vs RLUSD vs PYUSD)

- Stablecoin Types 2026: Fiat-Backed vs Crypto-Backed vs Algorithmic — What Each Actually Backs

- Stablecoin ETF 2026: The 3 Categories Investors Confuse (Tokenized MMFs vs Equity ETFs vs Pending Direct Funds)

- Cheapest & Safest Way to Buy ETH with Stablecoins on a DEX (2026): Real Fees, Gas Without ETH & Scam Defense